Schlüsselbegriffe: Forstliche Testbetriebsnetze, Informationsnetz landwirtschaftlicher Buchführungen, Diversifikation, Resilienz, Beratung, Kleinwaldwirtschaft

Abstract

Assessing the economics of small-scale farm forestry (SSFF) is associated with typical challenges. There is a large number of economically small or even very tiny although quite diverse institutional units with hardly any standards in terms of bookkeeping. At the same time, there is a multiplicity of more or less interrelated on-farm activities, forestry being only one kind-of-activity within the institutional unit. In North as well as in South Tyrol farm forestry is investigated in terms of full cost accounting applied to small and purposively chosen sub-samples of the respective national Farm Accountancy Data Network (FADN). These forest accountancy networks (FANs) allow eliciting the contribution of forestry to family income. Additional data collected and analyzed for this purpose enables us to quantify the significance of forestry for the Total Economy of Farm (TEoF). Full cost accounting for all on-farm activities, as performed in South Tyrol, is advocated as a starting point for investigating interrelationships between the kind-of-activity-units within one institutional unit and ultimately for optimizing the portfolio of the individual farm in regard to income and resilience. Respective insight is not only of scientific interest but may provide also valuable references for extension services and can help to improve sector statistics, where the major part of farm forestry is doomed to be regarded as inseparable non-agricultural activity.

Zusammenfassung

Die Untersuchung der ökonomischen Verhältnisse bäuerlicher Kleinwaldwirtschaft sieht sich mit typischen Herausforderungen konfrontiert. Einerseits handelt es sich bei der Grundgesamtheit um eine große Zahl ökonomisch sehr kleiner, institutioneller Einheiten, die aber durchaus individuelle Charakteristika aufweisen und überwiegend nicht über systematische Aufzeichnungen im Sinne einer Buchhaltung verfügen. Zudem ist man regelmäßig mit mehreren verschiedenen, wirtschaftlichen Tätigkeiten konfrontiert, die im Verbund des Hofes verfolgt werden und die in unterschiedlichem Maße untereinander in Wechselwirkung stehen. In Nord- und Südtirol wird die bäuerliche Kleinwaldwirtschaft im Sinne einer Vollkostenrechnung mittels spezifischer Testbetriebsnetze untersucht. Dabei handelt es sich um kleine, bewusst ausgewählte Substichproben des Informationsnetzes Landwirtschaftlicher Buchführungen. Neben dem forstlichen Betriebsergebnis, das den Beitrag der Forstwirtschaft zum Familieneinkommen in Geldeinheiten quantifiziert, erlaubt es die Datenlage, auch den relativen Anteil des forstlichen Betriebszweiges als Teil aller Wirtschaftsaktivitäten am Hof darzustellen. Für die Analyse von Wechselwirkungen zwischen den Betriebszweigen und letztlich auch für die Optimierung des entsprechenden Portfolios nach Maßgabe von Einkommen und Resilienz wird eine Vollkostenrechnung für alle Betriebszweige empfohlen, so wie sie im Südtiroler Netzwerk bereits praktiziert wird. Daraus gewonnene Erkenntnisse sind nicht nur von wissenschaftlichem Interesse, sondern könnten auch der Betriebsberatung zugutekommen. Darüber hinaus birgt die Vollkostenrechnung für den forstlichen Betriebszweig auch Potenzial zur Verbesserung der Agrarstatistik, wo die bäuerliche Waldwirtschaft bislang ggf. als nicht trennbare, nicht landwirtschaftliche Tätigkeit enthalten ist.

1. Introduction

Farm forestry enterprises (FFEs) represent entities, where individuals, families or corporations are engaged in agriculture as well as in forestry (Peck and Korotkov, 1991). The combination of agriculture and forestry within an institutional unit (the farm) is especially typical for the alpine region and is vital for the provision of various ecosystem services, the safeguarding of diversified cultural landscapes as well as for the rural economy. In terms of Europe as a whole, small scale farm forestry enterprises are currently encompassing 16 million private forest owners (CEPF, n.d.) who manage 60% of the EU's forest land (Eurostat, 2017). The bulk of the forest properties (99%) is smaller than 50 ha. In 2000, 59% of Europe’s forest owners were already 60 years or older (Schmithüsen and Hirsch, 2010). Although they are the largest group of forest owners, they are the least noticed and politically represented ones (Labarthe and Laurent, 2013). Triggered by demographic and economic developments, there is a general shift from active farm management towards various practices of so-called new forest owners (Hogl et al., 2005; Weiss et al., 2019), including even abandonment. ‘New’ owners sometimes even do not know where their forested land is located, the forest administration is not always informed, whether they still manage their land or whether they generate a periodic income (Schmithüsen and Hirsch, 2010). There is also a general trend towards part-time farming, where an off-farm employment is necessary in order to sustain a viable household income (Darnhofer, 2010; Darnhofer et al., 2016; Evans and Llbery, 1993; Weltin et al., 2017).

Mainly the findings from the agro-structural change in the Alps triggered the insight that there is a need for intervention on the policy level. Between 1980 and 2010, up to 80% of the farms have abandoned their activities in some parts of the Alps. Compared to these extreme figures, the abandonment rates in our case study areas of South- and North Tyrol, which vary between 15% and 25%, are quite moderate (Hoffmann et al., 2010; Niedermayr et al., 2015; Streifeneder, 2010; Streifeneder et al., 2007). Nevertheless, the management especially of less favored sites with low productivity in marginal areas that have to cope with an over-aging population is at stake (MacDonald et al., 2000; Navarro and Pereira, 2015; Rey Benayas, 2007). Across Europe, the obsolescence of the population of these remote and marginal rural areas is associated with a population decline of 4,9% between 1997 and 2017 (FAOSTAT, 2020). Abandonment is likely to impact on the various ecosystem services. However, these interrelationships are insufficiently understood so far and a limited number of studies address such issues (e.g. Conti and Fagarazzi, 2005). Additionally, the uncertainty, who owns the forest, the remoteness and the unavailability or the lacking organization of forest owners makes it difficult for authorities to apply or enforce regulations (Secco et al., 2017; Stampfer et al., 2001). This becomes particularly evident in the case of biotic or abiotic disasters. If technical or human resources from forest owners are lacking and if forest policy and its institutions are not capable to access them to intervene appropriately (Lawrence, 2018) these damages coupled with a reluctance to restore the forest could significantly endanger certain forest ecosystem services, in particular the protective functions (Kulakowski et al., 2017). Moreover, the consequential damage of these events, triggered by insects or further strong wind events, would even raise the vulnerability of the remaining forest stands (Dupont et al., 2015; Gardiner et al., 2013).

Precisely because of such scenarios, which are also perceived by the general public, the forest has recently been able to attract the attention of politicians and to become more prominent in Europe’s New Green Deal (EFI, 2020). Unfortunately, the policy measures of the “New European Forest Strategy” which is aligned with the new European Biodiversity strategy, are mainly focusing on the societal interest in various forest eco-system services, thereby neglecting the problems of forest owners in managing their forests sustainably (Hetemäki, 2020).

Therefore, it is that much important to signal to actively managed FFEs how significant their contribution is in this political context and to assist them in their efforts to sustain their economic viability and resilience. To be credible here it is essential to know the economic conditions of these farms. In this context, we specifically address the role of forestry. Economic analysis of farm forestry, be it for supporting decision making by owners or managers, driven by scientific interest or for statistical purposes, has to rely on information and ratios based on some kind of accounting data. In principle, financial accounting and managerial accounting are to be distinguished. Tax regulations and other legislation define the type of bookkeeping required as well as the business unit to be addressed in terms of financial accounting. In most cases, financial accounting refers to the farm as a whole. At any rate, agriculture and forestry adhere to the same category of income, so that no respective differentiation is required on formal grounds. Conversely, managerial or cost accounting is a voluntary exercise for addressing issues of efficiency in more detail and can be perceived as an extension of financial accounting. The distinction of cost centers within a company and assigning monetary values to unpaid inputs and outputs such as family labor and in-house-consumption are typical features of managerial accounting. Clearly, the economic analysis of farm forestry requires a database in terms of managerial accounting specific for the forestry part of the FFE. In practice, however, hardly any accounting data is generally available at farm level, most FFEs being subject to total or partial lump-sum taxation so that no financial accounting is required (Jilch and Kaluza, 2011; Urban, 2011).

Voluntary bookkeeping is therefore the key to economic insight into farm forestry. Although Forest Accountancy Networks (FANs) have a long tradition as an approach for monitoring economic figures and their development (Toscani and Sekot, 2018) and FFE-specific guidelines have been developed in the late 1990-ies (Niskanen and Sekot, 2001), such research infrastructure is still extremely rare, Baden-Württemberg providing an exceptional and most interesting example (Brandl, 2011). However, at least all member states of the EU are running a Farm Accountancy Data Network (FADN) as generally required by EU-regulations. This infrastructure for farm research is a plausible starting point for investigating the economics of farm forestry. Unfortunately, the FADN as such does not satisfy information needs in terms of forestry economics. It focusses particularly on agricultural activities and does not picture any other business fields applied at farm level (EC, 2018a). Therefore, forestry extensions in terms of contents and – as dependent from the population of interest – potentially also in terms of the sampling frame are required. Hence, an FAN monitoring the economics of FFEs may be established in terms of an extension of an FADN where the investigated holdings provide additional, forestry-specific information.

In this paper, we refer to two case studies, where an FAN is operated on the basis of the national FADN. We demonstrate at the example of two alpine regions, how the FAN-concept can be developed into a holistic “Total Economy of Farm” (TEoF) approach. For this purpose, the accounting system has to document the different business units specifically. This should enable farmers to address the interrelationships between the different lines of business of their diversified farms and to identify operational bottlenecks at an early stage. Furthermore, the continuous analysis of aggregated data should lead to relevant information for policy-makers and extension agencies. The growing theoretical insight into the economics of farm forestry together with empirically based references shall help to design innovative development pathways for FFEs.

The authors were engaged in designing, implementing, running and analyzing two FANs addressing farm forestry and want to share their experiences especially as regards the innovative TEoF-aspect. Our investigation is devoted to that segment of small-scale farm forestry, where land management is the major source of income and forestry is a significant line of business besides pasture-based feedstock-farming. In 2017, Eurac Research started a cooperation with the University of Natural Resources and Life Sciences, Vienna (BOKU) in order to establish an FAN in South Tyrol. This pilot project was specifically designed to address and investigate farm forestry in the context of TEoF. The main motivation for this initiative was to give common answers to the driving research question: “By what means may rural entrepreneurs and the advisory service assess the significance of forestry for the viability and resilience of diversified alpine farms?” Furthermore, we deal with the research question ‘How can an existing FAN be extended towards assessing TEoF?’ at the example of Austria.

2. Material and Methods

We present the approach and results of FAN-exercises in Austria (with special consideration of a sub-sample located in North Tyrol) and South Tyrol (belonging to Italy). Following an explorative approach, panels were selected out of the FAN-sample of each region. Thus, all units of investigation have been consistently surveyed in the years 2017 and 2018. By considering the period-specific distribution of expenses and revenues, also in case of discontinued harvesting, we derive our results from the cost object accounting with absolute and relative economic indicators for each operating unit. The synopsis of two accounting periods enables us to compare each unit across-periods and to apply a comparative analysis with the mean values derived from the South Tyrolian sample. By adding the mean values from North Tyrolian panel of farm forests from the same periods, we extend the analysis to a cross-border comparison. Additionally, the Austrian data are analyzed in regard to averages and developments for two decades, thereby comparing the all-Austrian panel with the respective panel of North Tyrol.

2.1 Theoretical Framework

A sound business strategy for a farm has to rely on a thorough assessment of all resources available and their potential for utilization, thereby considering trade-off-relationships and related opportunity cost as well as synergies. Ultimately, an individual portfolio of activities and related business units should allow to optimize TEoF. Although the European Commission approved the project MOSEFA – Monitoring the socio-economic situation of European farm forestry in 1997, there are still only few studies dealing with the methodological aspects of FANs. In the few cases where an FAN is operated a purpose-specific, sector-orientated accounting approach is applied. Rarely, they address diversification in terms of a synopsis of all business units operated at farm level. However, the viability of a farm has to be addressed at household level (Niskanen and Sekot, 2001).

Factor-income per annual work unit, as applied in national agricultural and forestry accounting, refers to the income of a statistical person employed full-time in agriculture or forestry respectively. It is a very broadly defined indicator that includes income from dependent employment, income from self-employment as well as profits (net business income), rents and earned interest. Although reflecting broadly the national agricultural household income in the long-term perspective, the national agricultural factor income is not an appropriate indicator for the specific living conditions of the farm manager and co-working family members (Sinabell, 2013). In principle, the national statistical reports for agriculture and forestry that are collected by EUROSTAT, aim to determine the income generated by the respective activities. These statistics follow the ‘kind-of-activity-unit’ approach, where farms as institutional units are subdivided according to the different economic activities. However, where farm forestry is of minor importance, this differentiation is not necessarily applied, and farm forestry may be included in the agricultural accounts under the term of ‘inseparable, non-agricultural activities’.

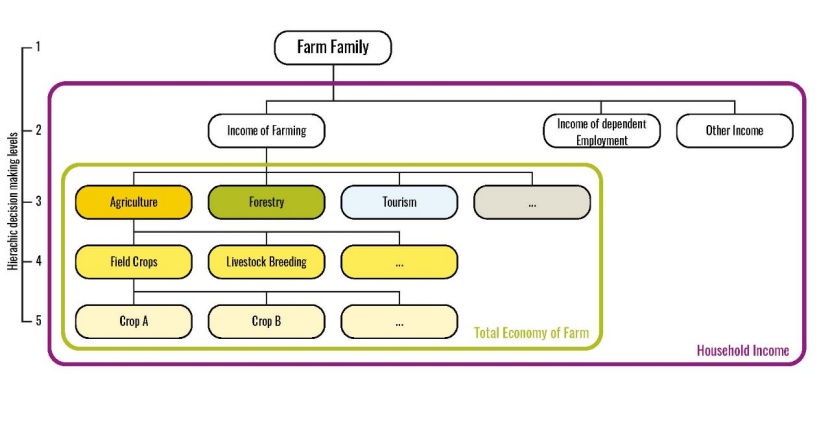

Figure 1: The applied 'Total Economy of Farm' concept with it's different levels of hierachic decision making on the basis of Niskanen and Sekot (2001) and Mutenthaler and Sekot (2016). / Abbildung 1: Das verwendete ‘Total Economy of Farm’ Konzept mit seinen unterschiedlichen hierarchischen Entscheidungsebenen in Anlehnung an Niskanen und Sekot (2001) und Mutenthaler und Sekot (2016).

The national FADN is a major source of data for sector statistics. Although it has to comply with common international standards, specific extensions may be considered. In Austria, the so-called ‘Green Report’ (BMLRT, 2020) provides on an annual basis detailed data concerning the total income of farm households. The underlying network of voluntarily bookkeeping farms acknowledges unpaid family labor and records also any income from off-farm activities by household members. It is thus a most valuable database for investigating the viability of rural households (Sinabell, 2013). But even the Austrian FADN shows limitations as regards the TEoF-concept. Only revenues from agriculture and forestry are documented specifically, whereas, any other revenues of diversified farms are aggregated to “other revenues from secondary activities”. Furthermore, the expenditures are not differentiated according to activities. Consequently, a detailed reporting on the performance of an individual line of business is hardly possible (BMLRT, 2020). Accordingly, we cannot verify at first sight, whether the generated earnings of each business line contribute positively to the household’s income or if that unit is in fact subsidized by the others. Keeping these limitations in mind, we demonstrate the potential of the existing data for addressing the significance of farm forestry in terms of TEoF. For this exercise, we merge the data of the Austrian SSFN with the FADN-database. Conversely, the FAN in South Tyrol applies the TEoF-concept directly as well as comprehensively. Figure 1 illustrates the TEoF concept.

The term household income in common definitions (e.g. OECD (2013), UNECE and CES, (2011)) comprises all annual or more frequent receipts received by a household or its individual members. It is traditionally used for both, macro statistics at national levels and micro statistics of different socio-economic groups (UNECE and CES, 2011). In contrast, the TEoF concept focuses on accountancy data, comprising various business units managed at a farm, which are using existing assets and are managed on own-account (e.g. agriculture, forestry, farm holidays). Income from dependent employment, other revenues e.g. renting of land and financial income are not addressed. All business units are analyzed individually, thus accounting data must be allocated specifically.

2.2 Full cost accounting in farm forestry

In the study areas, we are in the lucky position to have the possibility for applying full cost accounting. Joint costs and overheads are differentiated by means of specific keys such as the share of working hours or the ratio of forestry and agricultural tax-values of the property. In Austria, all jointly used fixed assets such as machinery are individually assessed, the so-called ‘forestry-factor’ giving the percentage, to which the asset and associated cost are assigned to forestry (BMNT, 2018a). The imputed value of family labor is assessed using hourly wage rates and the recorded working hours for each business unit. The following differences in terms of methodology have to be noted, however: In the Austrian SSFN, the effective working hours of all unpaid labor are recorded per cost center. The average wage rate for the two years in question was 24.58 €/hour with harvesting and 14.90 €/h for all other forestry work. In the FADN, effective working days per person are documented per kind of activity such as agriculture, forestry or farm holidays. This gives a theoretical maximum of 2920 working hours per person, as each working day represents 8 hours (BMNT, 2018a). Conversely, in ST a number of 1680 working hours per year was taken as a reference for calculating, in alignment with the farm managers, the share of work force dedicated to any applied business unit beyond agriculture. By referring to the “Collective Contract” for agricultural workers of the South Tyrolean Farmers' Union, the standard remuneration per working hour was distinguished between the entrepreneurial farm manger (15,92€/h, 2018) and for the collaborating family members (14,12€/h, 2018). By doing so, the forestry-share as well as the share for any other applied business unit at a farm got individually assigned for each analyzed sample.

2.3 Accountancy Data Networks and investigation areas

To evaluate the income of agricultural holdings as well as the impact of the Common Agricultural Policy, the European Commission established the FADN in 1965. On an annual basis harmonized accountancy data from a sample of farms is collected in all member states (EC, 2013). In principle, the entire range of agricultural activities on farms is addressed by the FADN survey, including tourism and forestry but without differentiation between lines of business in terms of profitability (EC, 2018b). In order to address the economics of forestry in several European countries FANs were developed independently enabling the monitoring of the socio-economic situation of forestry (Toscani and Sekot, 2018). The countries of the so-called DACH region (Germany, Austria, Switzerland) share the longest tradition with more than six decades of experience (Sekot, 2011). Accountancy Data Networks in general, have 3 tasks: describing the current socio-economic situation and interpreting the results, deriving forecasts and providing indicators for decision making (Dög et al., 2018). The availability of accountancy data in the two regions under investigation in this study is outlined below.

Investigated data from Austria

Austria, being a member of the European Union, is operating an FADN comprising a quota sample of around 1,960 farms (BMLFUW, 2017, 2016; BMLRT, 2020; BMNT, 2019, 2018b). Due to the great significance of farm forestry in Austria, the national FADN exceeds the European requirements in terms of sampling frame and content. Consequently, more than 80% of the Austrian farm forests are represented by the Austrian FADN. Although some extensions of the dataset were made in recent years (Toscani and Sekot, 2015), the delimitation of inputs for a farm´s different business units is only possible to some extent. At least regarding the forestry branch of farms in-depth information is provided by the SSFN. The SSFN is in fact a purposive subsample of the FADN comprising about 110 farms managing forest land between 5 and 200 ha that provide supplementary information about forestry costs and revenues (Hyttinen and Kallio, 1998; Toscani and Sekot, 2017). The SSFN is a separate investigation and the datasets for agricultural and forestry purposes are not integrated. As the SSFN provides data since 1972, it is well established and according to Hartebrodt and Hercher (2012) in a phase of extended data provision. Whereas results derived from the FADN are representative for the roughly 76,000 farms covered by the sampling frame (49.1% of all farms) (BMLRT, 2020), the SSFN is biased towards bigger forest holdings so that representative results cannot be derived (Sekot, 2001; Toscani and Sekot, 2017, 2015). From 1994 onwards, a set of about 40 figures ranging from farm characteristics to monetary results out of the agricultural database is adjoined to the units of investigation in the SSFN. The intention has been to lay the basis for further analyses such as addressing forestry in the context of TEoF. Such an analysis is done here for the first time, thereby referring to a panel of 56 holdings covering the time-span from 2000 to 2019. The analytical potential of fully merged agricultural and forestry datasets is demonstrated at the example of North Tyrol (NT) which has been selected for cross-border comparison. In total 13 farms in NT could be identified that provided data for the investigated fiscal years 2017 and 2018. At average these 13 farms manage 32.6 ha agricultural land and 24.0 ha forest land. The 20-year-panel of NT comprises 7 farms.

Investigated data from South Tyrol

Italy, as well being a member state of the European Union, is also operating an FADN to monitor the socio-economic conditions in agriculture. Unlike in Austria, an extension towards forestry specific data is not implemented (Marongiu et al., 2012). Although some research effort has been undertaken (Marongiu et al., 2012), a specific FAN has not been introduced yet (Toscani and Sekot, 2018). To improve this situation at least in South Tyrol (ST), the implementation of an FAN started in 2017. A purposive sample of around 15 farms is being monitored starting with the fiscal year 2017 (Toscani et al., 2018). It is in fact also an extension to the FADN as the observed farms are selected from the sample of voluntarily bookkeeping farms. In contrast to the SSFN in Austria, this network comprises all business units of a farm, following the TEoF concept. Due to fluctuation in the sample, 13 farms contributing to the South Tyrolian FAN in the fiscal years 2017 and 2018 could be investigated, so that – merely by chance – the size of the panel is identical in both regions. At average, the investigated farms manage 13,7 ha agricultural land and 43.9 ha of forest land.

2.4 Statistics

The numerical results do not claim representativeness in any way as they stem from very small and purposively selected samples. They just exemplify how the practical application of the TEoF-framework may trigger additional insight into small-scale farm forestry. The empirical findings are of indicative character and may inspire theoretical considerations but are as such not suited for any advanced analytical treatment such as the testing of hypotheses. Consequently, we present the results in terms of descriptive statistics, mainly as averages. The presented results are calculated considering all records as branches of one big farm. The mean value is calculated as the sum of all values x (e.g. forestry revenues) divided by the sum of all values of y (e.g. forest land) (Toscani and Sekot, 2015). Accordingly, the values show the average share of this branch on the farms´ total.

As regards the two 20-year-panels of the Austrian FAN, we compare respective characteristics and developments and just hint at the analytical potential of such time series in terms of correlation analysis. The correlation coefficient ‘r’ according to Pearson with numerical values between -1.0 and +1.0 is a measure of the direction and intensity of interrelationships. The square of the correlation coefficient (r2) is a coefficient of determination and indicates, which share of the variation of one variable is explained by the variation of the other.

3. Results

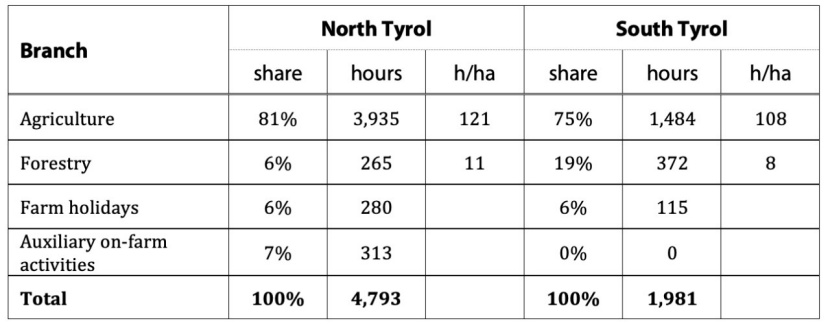

Table 1: Distribution of average familiy labor to the single branches of a farm in the fiscal years 2017 and 2018, displayed as a proportion (%), in total hours and in hours per ha (h/ha). / Tabelle 1: Verteilung der durchschnittlichen Familienarbeit auf die einzelnen Betriebszweige für die Wirtschaftsjahre 2017 und 2018 als Anteil und in Gesamtstunden sowie in Stunden je ha.

3.1 Distribution of family labor

Whereas the average number of family working forces at a farm in terms of capita differs slightly (3.7 in NT, 3.3 in ST), the sum of annual working hours spent with on-farm activities is 2.4 times higher in NT than in ST, as shown in table 1.

For the examined samples, agriculture is obviously the main branch in both regions. The share of forestry is in ST three times higher than in NT, corresponding to a higher share of forestry land (76.2% in ST and 42.4% in NT). In both regions, the input of family labor per ha is in agriculture ten times more than in forestry. The average family working hours for farm holidays are about 2.4 times higher in NT than in ST. Even more working hours were spent for auxiliary on-farm activities in NT, whereas for the remaining branches in ST almost no working hours were documented. For reasons of consistency, the figures for NT are calculated on basis of the FADN-dataset for all branches. Labor input in forestry appears to be about one third less when referring to the SSFN-data (172 hours as compared to 265 hours per year) which is a clear indication of methodological inconsistency.

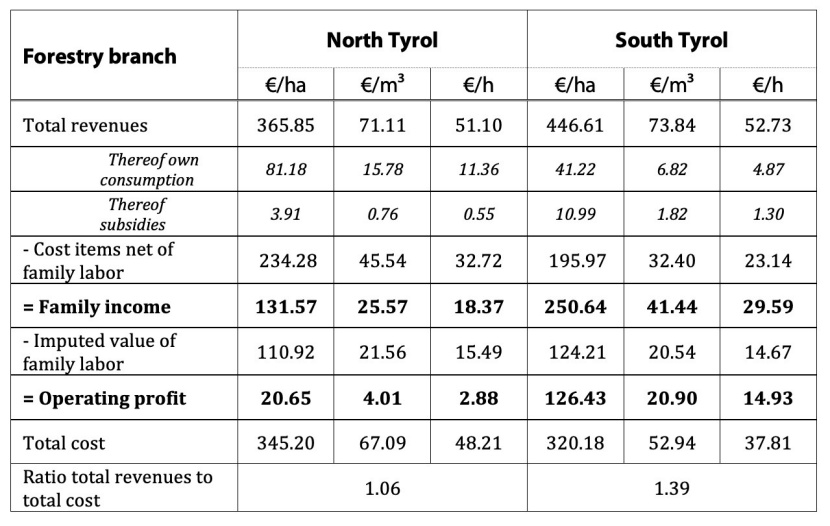

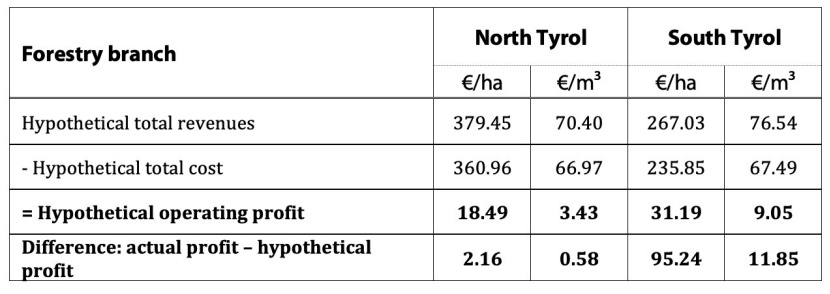

Table 2: Calculation of family income, operating profit and the ratio of total revenues to total cost for the average forestry branch in NT and ST. / Tabelle 2: Berechnung des durchschnittlichen Familieneinkommens, Betriebserfolgs und des Verhältnisses von Ertrag zu Kosten für den forstlichen Betriebszweig in NT und ST.

3.2 Income from forestry

Family income is the most significant indicator of profitability in farm forestry. By imputing the cost of family labor using specific wages (e.g. based on collective agreements), the operating profit for a whole farm or a single branch can be derived as shown in table 2.

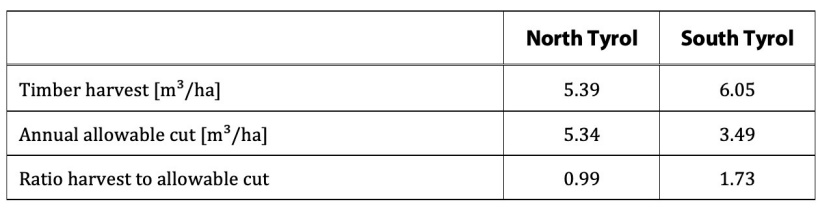

Table 3: Average annualy harvested timber and allowable cut for the investigated enterprises in NT and ST. / Tabelle 3: Durchschnittlicher jährlicher Holzeinschlag und Hiebsatz der untersuchten Betriebe in NT

At average, a positive operating profit results in both regions. Correspondingly, the ratio of total revenues to total cost exceeds the threshold of 1.0. Numerically, cost efficiency is considerably higher in ST as compared to NT. Such a finding is not suited for judging the quality of management, however. Additionally, the level of harvest has to be considered as it affects revenues as well as cost and profit can be increased by depleting the growing stock. Respective indicators are presented in table 3.

Table 4: Hypothetical results for a harvesting intensity corresponding to the allowable cut. / Tabelle 4: Hypothetische Ergebnisse bei Nutzung in Höhe des Hiebsatzes.

The intensity of harvest differs less than 20% between NT and ST. Greater differences can be observed in regard to the cutting ratio which relates harvested timber to the allowable cut. This ratio, if clearly exceeding 1.0 over a period of forest management planning, indicates a likely unsustainable utilization of the forest resource. In general, one of the major factors in pushing this ratio is unplanned, sanitary felling. Unfortunately, the share of sanitary fellings is not recorded by the FANs themselves. The regional record of cuts for small-scale forestry in NT may serve as a surrogate and documents a share of sanitary felling of 28.2% in 2017 and 33.1% in 2018, both figures exceeding the average of the decade before (26.9% for 2007-2016) (BMLFUW 2008…2015; BMNT 2016…2018). Harvesting statistics for all of ST quote 20.6% as the average share for the decade 2007-2016 as compared to 10.5% in 2017 and 30.2% in 2018 (Autonome Provinz Bozen – Südtirol 2020). These surrogates provide no hint for explaining the different levels of harvesting in NT and ST. In North Tyrol, harvest and allowable cut appear quite balanced. However, the specific ratios of 1.31 in 2017 and 0.70 in 2018 indicate the short-term volatility of this ratio as triggered by the respective cutting volumes.

A model calculation assuming a volume of harvest at the level of the annual allowable cut as well as fixed costs of harvesting and fixed timber proceeds per m3 highlights the effect of over- or undercutting in monetary terms.

The ratio of total revenues to total cost is hardly affected in North Tyrol (1.05 versus 1.06), whereas a major reduction can be observed in South Tyrol (1.13 as compared to 1.39). The difference between actual and hypothetical profit is an indication as to what extent the growing stock has been depleted or augmented in monetary terms.

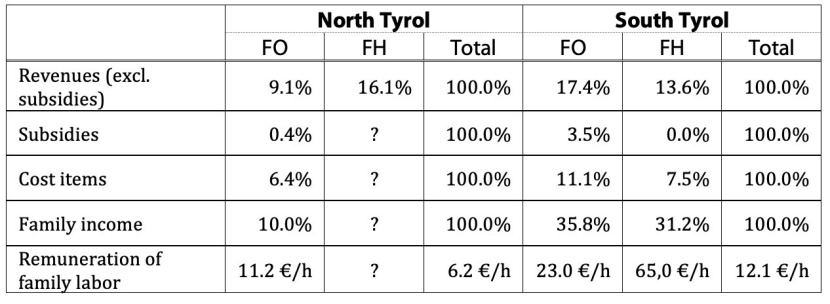

Table 5: Share of the forestry (FO) and farm holidays (FH) branch on the farm´s total revenues, subsidies, costs items and family income as well as the family income per unit of unpaid labor input in NT and ST. The symbol ? indicates a knowledge gap. / Tabelle 5: Anteil der Betriebszweige Forst (FO) und Urlaub am Bauernhof (FH) am gesamten Ertrag, Förderungen, Kosten und Reinertrag sowie das Familieneinkommen je nicht entlohnter Arbeitsstunde in NT und ST. Das Symbol ? weist auf Dokumentationslücken hin.

3.3 Total Economy of Farm

The application of the TEoF concept allows a comparison of a farm´s different branches at different levels. In table 5, an overview of selected shares of the branches forestry and farm holidays on the farm´s total for NT and ST is presented. As the used FADN data in NT does not allow a differentiation of inputs according to the different branches except forestry, NT suffers from knowledge gaps marked with the symbol “?”. With 9.1% of the revenues and 6.4% of the costs, the forestry branch produces 10.0% of the family income in NT. In ST more than a third of family income (35.8%) is produced by forestry. When calculating the remuneration of family labor by dividing the family income through the recorded working hours, it is almost twice as much in the forestry branch as the farms average in NT and ST.

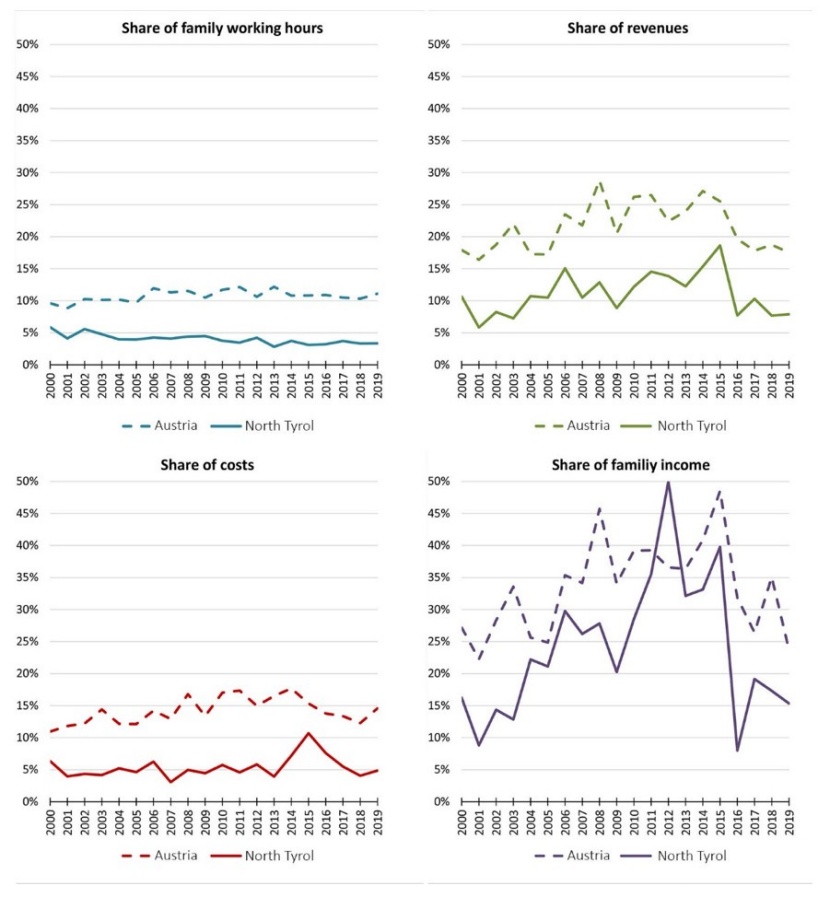

Figure 2: Development of the forestry branches´ share of the farms family working hours, revenues, costs and family income in NT and Austria. The underlying data stems from a panel of enterprises delivering data to the SSFN for all 20 periods from 2000 to 2019. / Abbildung 2: Entwicklung des forstlichen Anteils an den gesamten Familienarbeitsstunden, Erträgen, Aufwänden und Familieneinkommen für Nordtirol und Österreich. Die Ergebnisse entstammen einem Panel von SSFN Betrieben, welche für alle 20 Perioden von 2000 bis 2019 Ergebnisse dokumentieren.

The analytical potential of the TEoF concept, in terms of long-term observations of a sample of farms is indicated at the example of Austria in figure 2 and table 6. The graphs show the development of the forestry branches´ shares of the farms’ family working hours, revenues, costs and family income. In almost every observed fiscal year the relevance of the forestry branch in the observed units in NT is lower than the Austrian average. The 20-year average contribution of forestry to the family income is 23.5% in NT and 33.9% in Austria. This relates to a share of just 4.2% of the input in terms of family working hours in NT and 11.2% in all Austria. The framework of the Austrian FADN allows even to address the significance of off-farm sources of income, thereby extending the TEoF-scheme to the household level. On average, the share of off-farm income amounts to 10.0% according to the SSFN-panel for 2000 – 2019. In NT, the respective figure is less than half (4.5%).

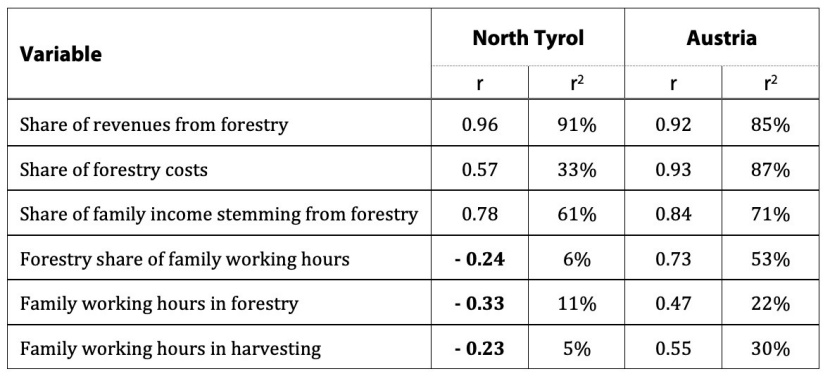

Table 6: Correlation analysis in regard to the volume of harvest based on panels for 2000 – 2019 (r … Pearson‘s coefficient of correlation; r2 … coefficient of confonfidence in %). / Tabelle 6: Korrelationsanalyse in Bezug auf die Nutzungsmenge für Panels des Zeitraums 2000 – 2019 (r … Korrelationskoeffizient nach Pearson; r2 … Bestimmtheitsmaß in %).

Correlation analysis marks a first step towards analytical statistics. The Austrian database allows to identify and analyse panels of farm forest enterprises for different time frames. As an example, respective results for the period from 2000 to 2019 characterizing the interrelationship between the volume of harvest and other variables are provided in table 6.

In general, there is a quite strong, positive correlation between share of revenues, share of costs and share of family income on the one hand and the level of harvest on the other. Quite remarkable is the slightly negative correlation between family working hours in absolute as well as relative terms and harvest in NT. One may just speculate, that this small group of farms tends to substitute family labor by contractor’s work in periods of especially high harvest, whereas a moderate, positive correlation prevails at the all-Austrian level.

Table 7: Stepwise calculation of the average family income and operating profit for the different branches of the investigated enterprises in ST. Monetary values in 1,000 € per farm. The abbreviations are AC Agriculture, FO Forestry, FH Farm holidays, PV Photovoltaics, RE Renting of estate, SU Supply of services, WC Wood chip energy production and NE Neutral. / Tabelle 7: Schrittweise Berechnung von Familieneinkommen und Betriebserfolg der jeweiligen Betriebszweige der untersuchten Betriebe in ST. Monetäre Werte in 1.000 € pro Betrieb. Die verwendeten Abkürzungen sind AC Landwirtschaft, FO Forstwirtschaft, FH Urlaub am Bauernhof, PV Photovoltaik, RE Grundtücksnutzung, SU Leistungen für Dritte, WC Hackschnitzelanlage und NE Neutral.

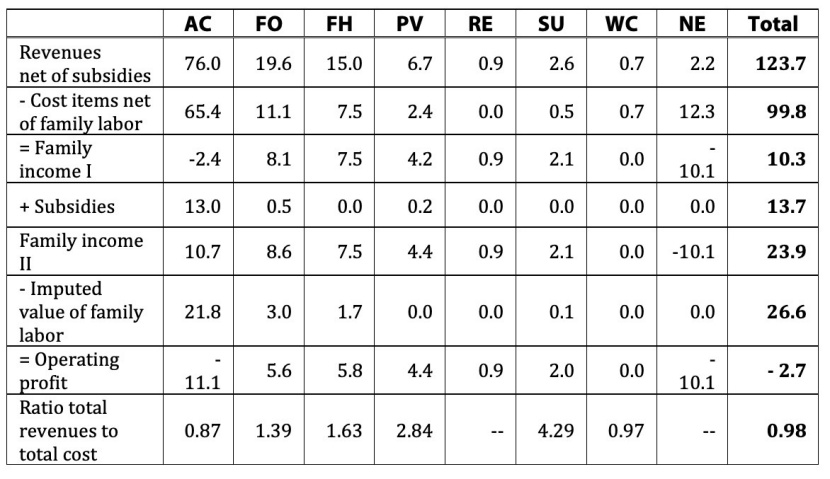

Table 7 gives some deeper insight into the farm´s income situation. A stepwise calculation of the family income, operating profit and the ratio of total revenues to total costs is performed. Due to the above-mentioned limitations, the presented results comprise the average values for ST only.

The biggest share of the average revenues belongs to agriculture (61.4%), followed by forestry (15.9%) and farm holidays (12.1%). Over 95% of a farm´s subsidies concern the agricultural branch. The distribution of the cost items follows the revenues, with the highest share (65.5%) in the agricultural branch, followed by forestry (11.1%) and farm holidays (7.5%). At average, all branches except agriculture and wood chip energy production produce positive family income when subsidies are excluded. The agricultural branch only turns positive, when subsidies are taken into account. Discounting the imputed value of family labor from family income leads to the operating profit. A negative operating profit, such as in the AC branch indicates, that the invested work force of family members does not earn the imputed hourly wages. The branches with the highest operating profit are farm holidays, forestry and photovoltaics. A further figure to compare the different branches is the ratio total revenues to total cost. Values above 1.0 correspond to a positive operating profit.

4. Discussion

The numerical results show a significant difference in terms of labor input which consequently affects all related ratios. A plausible explanation for at least part of this difference at farm level is the significantly higher acreage of agricultural land in NT. Especially in regard to the forestry results, the different way of assessing working hours of unpaid labor as described in the methods’ section have to be taken into account. Hence, one must not jump to conclusions in terms of efficiency but has to interpret findings prudently before the background of possibly or even effectively inconsistent methodology. We have to acknowledge a lack of comparability in this respect. On top of that, it has to be annotated, that in NT, the information in regard to forestry differs between the dataset of the FADN, which has provided the results presented in table 1 and the figures of the SSFN which were used for calculating the ratios documented in table 2.

The Austrian time series in figure 2 illustrate the variability of different ratios and thus underpin the significance of averages calculated over a multiplicity of periods. The different levels of correlation are in line with the general consideration, that farmers allocate a certain time budget per year for forestry activities more or less independent from the level of harvest. It can be presumed, that extraordinary cutting volumes, especially when triggered by calamities, are met by an additional input of contractors’ work.

A further finding of the empirical results is the discrepancy between the family income and the operating profit in table 7. A negative operating profit while positive family income means, that the imputed wages for family labor could not be earned. A recent study by Kirner et al. (2020) for selected Austrian farms shows big differences in the effective hourly remuneration between the branch farm holidays and direct marketing. An effective hourly remuneration for family work below legal minimum wages means, that it would not be possible to outsource this kind of work without an increase in efficiency. However, family income or the hourly remuneration of family labor is just one option to measure the efficiency of a specific business line. The owner of a farm may also define a requested Return of Investment (ROI), Return on Equity (ROE) or Return on Sales (ROS) at farm-level with a further brake down to each business line.

Furthermore, for the interpretation of the numerical results it has to be kept in mind, that in the investigated units in NT and ST the agricultural branch is dominant in terms of revenues, cost and working hours of family members. The occurrence of a clearly dominant business line may trigger systematically biased estimates. For the observed farms in ST it is not verified yet, whether non-dominant branches are associated with correct or biased shares of overheads and labor input. The TEoF concept as presented in this study uses longitudinal socio-economic data, stemming from the respective accountancy data networks. Despite of a well established FADN and FAN in NT, the extension towards the TEoF concept is limited to the delimination of forestry from all other on-farm activities. Whereas outputs can be allocated to most of the other branches, it is not possible for the inputs. Only for the forestry branch an allocation of joint overheads based on the share of the assessed tax values (BMNT, 2018a) is possible. Thus, to apply the TEoF concept in NT further recordings would be required as performed in a study by Kirner et al. (2020). In ST the newly established FAN was designed following the TEoF concept. Thus, for all branches the specific inputs and outputs are recorded and joint overheads are allocated based on an estimation on behalf of the farmers.

The case studies inspired also quite general considerations as to the economic analysis of farm forestry which may be of interest in another context and serve as an empirically founded supplement to the MOSEFA-guidelines. A core challenge is to establish a specific documentation in terms of managerial or cost accounting. One possibility is to basically apply the elements and ratios of financial accounting to the forestry part of the company as recommended e.g. by Penttinen and Hakkarainen (1998) and Hyder et al. (1999). However, a delimitation of all inputs and outputs is a pre-requisite for that approach as well as for full cost accounting. For gaining at least some insight into the economics of farm forestry starting from voluntarily kept records for the whole farm, we propose to consider a stepwise approach. Some factors of production such as seedlings or specific tools as well as the majority of revenues e.g. from selling timber can be considered as exclusive for forestry. Addressing and recording these elements specifically would be the first step. A sub-division of type of cost may augment forestry-specific information. In Austria, for instance, a differentiation of services rendered by contractors into agricultural and forestry-specific ones has been implemented throughout the network of voluntarily bookkeeping farms. A further extension can be achieved by separately recording quantities of crucial inputs like the working hours of family labor (which is the case in the Austrian FADN) or machinery. Comprehensive direct costing requires the differentiation of all specific inputs according to cost centers, forestry being one of them. For full cost accounting, which provides a maximum of information and which is the approach underlying the data analyzed in this paper, the issue of overheads and joint costs has to be resolved. Niskanen and Sekot (2001) discuss the pros and cons of two alternative ways of dealing with joint costs. Merely recording joint costs in terms of separate cost centers e.g. for a tractor or a building would be insufficient in terms of full cost accounting, however. Several concepts for the allocation of joint costs and overheads exist using the principles of causation, cost recovery or cost unit accounting (Gazzarin and Lips, 2018). Blum (1994) suggests a negative selection of cost centers not charged with a certain kind of overheads before allocating the overheads to the remaining cost centers (Mantau et al., 2001).

A peculiarity of small-scale farm forestry is, that harvesting for selling timber is often not performed every year. This so-called intermittent harvesting is a very common management regime in farm forestry (Niskanen and Sekot, 2001). It is, in principal, also a form of sustainable utilization, but the preconditions for annual sustainable production are often not fulfilled (Oesten and Roeder, 2012a). Speidel (1984) assumed some 50 ha as a lower threshold for annual market-oriented harvesting but in practice the harvesting regime is affected by a bunch of frame conditions and is likely to be quite volatile. Beside the given production conditions, intermittent harvesting can also be seen as an intended management strategy in farm forestry. The key of this strategy is to produce timber only in times with economically favorable market conditions (Oesten and Roeder, 2012b). Furthermore, farmers often perceive and use standing timber as a ‘green savings deposit’ where major harvests are typically triggered by specific cash-requirements e.g. for financing investments. Whatever the reasons for intermittent harvesting in the forestry branch are, this management regime is challenging for economic analysis and strategic decision making. Whereas in a farm´s other branches the realized annual income is mostly the result of the input and output within one year, the output in forestry is decoupled from the input due to the long production periods of several decades. In a single fiscal year or a short period as observed in this study, timber harvesting and thus the contribution to a farm´s income might not be representative. In well-established datasets (e.g. SSFN in NT) the calculation of average values over a long time span leads to more reliable results (Sekot, 2007a). If there are just a few fiscal years documented, like in the recently established network in ST, other solutions are required. A simple way is to check the ratio of annual harvest to annual allowable cut, as presented in table 3. A value well above 1.0 indicates overcutting in the observed sample, whereas a value well below 1.0 means that the sustainable available potential is not fully tapped. For the observed farms in ST this ratio is 1.73, indicating that the income from the forestry branch in table 7 is positively biased. Possible reasons for this significant deviation have not been investigated yet and range from sanitary fellings due to desasters and specific economic frame conditions like timber prices up to possibly systematically underestimated figures of allowable cut. To address this problem, referring to the Austrian FAN for lager enterprises (Sekot, 2017; Toscani and Sekot, 2018), a model calculation can be used, which calculates the hypothetical profit gained by utilizing the annual allowable cut. Clearly, the validity of the results stemming from such a model calculation strongly depends from the quality of the underlying annual allowable cut. As in small-scale forestry management plans are rather an exception than the rule (Toscani and Sekot, 2018), surrogates like regionally defined levels for sustainability could be applied (Sekot, 2011). The results as documented in table 4 exemplify the application of such a model calculation. The small difference between the actual harvest and the allowable cut in North Tyrol must not be mistaken for an indication of a highly sustainable management, however, the level of the allowable cut per ha being a regional reference for small-scale forestry throughout Tyrol. Furthermore, even a holding-specific allowable cut quantifies the volume of sustainable harvest only and is as such not a reliable and valid indicator of economic sustainability. Other aspects like the pattern of tree species, assortments, timber quality, type of harvesting operations and terrain for harvesting should be addressed additionally (Jöbstl, 2000; Toscani and Sekot, 2018).

On-farm diversification as an option to boost resilience at farm level is an often-mentioned strategy (Ashkenazy et al., 2018; van Zonneveld et al., 2020). It might also be seen as an efficient risk management mechanism in an uncertain environment (McNamara and Weiss, 2005). But not all types of diversification strengthen farm resilience. They have to be evaluated in the context and, if possible, based on longitudinal studies or case studies of farm trajectories (Darnhofer, 2014). Diversification of farms can be supported in most business lines by subsidization as shown for the case of Austria by Sinabell et al. (2019). Lips and Schmid (2013) report a decreasing diversification of Swiss farms since the 1990ies. Within the last decade an increase of the relevance of branch accounting for practice and advisory services is reported (Gazzarin and Lips, 2018; Kirner et al., 2020). We maintain, that the application of the TEoF concept can support farmers and advisory services in evaluating the individual business units. Beyond that, this information backs decision making at farm level towards diversification and higher resilience or specialization and higher efficiency.

Sector statistics, too, may benefit from full cost accounting of farm forestry (Sekot, 2007b). The guidelines for the agricultural and forestry accounts (EUROSTAT, 2000) allow to treat farm forestry as inseparable non-agricultural activity. Consequently, farm forestry may be part of the agricultural accounts and may be missing in the forestry ones. E.g. in Austria, full cost accounting for all farm forests within the FADN is modelled based on parameters derived from the SSFN (Toscani and Sekot, 2014). The Statistics Austria Federal Institute is using results from this exercise for establishing the Economic Accounts for Forestry (Statistik Austria, 2020). Furthermore, the estimated figures of small-scale forestry are deducted from the farms’ total in order to derive the net figures of agriculture for the Agricultural Accounts (Statistik Austria, 2019).

5. Conclusions and Outlook

The TEoF-concept is an institutional approach following the line of thinking, that the whole is more than the sum of it’s components, the so-called kind-of-activity-units. Comprehensive full cost accounting for all the different lines of business would enlarge the basis for addressing operational as well as financial synergies (Hyttinen and Huovinen, 1998) but also trade-offs. We are well aware, that individual farmers will hardly apply accounting according to the TEoF-concept all on their own. However, extension services may induce and assist pilot applications and refer to these when rendering their services to other farmers (Sekot et al., 2017; Sekot and Toscani, 2020).

In this study, we investigate TEoF starting from existing FANs where full cost accounting is applied at least to forestry. For the time being, the approach in ST seems to be the leading edge as regards the possibilities to analyze farm forestry in terms of TEoF. The continuation of this exercise should allow to investigate developments and interrelationships between forestry and other lines of business and thereby also to address the phenomenon of intermittent harvesting even more specifically. Although an extension of the sample would be of scientific interest as well, the odds are not too promising in this respect. In the Austrian case, significant progress might be achieved by continuously coupling the forestry dataset with the entire information on the respective farms as documented in the FADN.

The availability of established FANs is quite exceptional, however. For other countries it may be of interest to derive forest-specific information by further differentiating agricultural investigations which address institutional units (=whole farms with their full portfolio of economic activities). Generally, more insight into the economics of farm forestry could be a by-product of refinements of agricultural investigations. However, in most countries, forestry- specific information based on existing FADNs would cover only the smaller part of farm forestry. Especially forestry-dominated holdings as well as very small properties will hardly be part of an FADN and thus would call for a respective extension of the sampling frame. Efforts in regional development could also trigger more insight into the economics of farm forestry (Hyttinen et al., 2000), especially in peripheral areas with significant forest resources managed by farms.

Acknowledgements

The authors would like to thank the Austrian Federal Ministry of Agriculture, Regions and Tourism for the provision of the FADN data and LBG Österreich GmbH for the additional information for merging FADN and SSFN data. Furthermore, the authors would like to express their sincere thanks to the IDM department "Wood & Construction Innovation", which financed the establishment of the FAN for farm forestry in South Tyrol. Finally, we also want to thank the South Tyrolean Farmers' Association, which supported us with providing the samples for the newly developed FAN from the voluntarily bookkeeping farms.

References

Ashkenazy, A., Calvão Chebach, T., Knickel, K., Peter, S., Horowitz, B., Offenbach, R., 2018. Operationalising resilience in farms and rural regions – Findings from fourteen case studies. Journal of Rural Studies 59, 211–221. https://doi.org/10.1016/j.jrurstud.2017.07.008

Autonome Provinz Bozen-Südtirol (Ed.), 2020: Agrar- und Forstbericht 2019. http://www.provinz.bz.it/land-forstwirtschaft/landwirtschaft/agrar-forstbericht.asp (accessed 14.4.21).

Blum, A., 1994. Zur Marktfähigkeit infrastuktureller Leistungen des Waldes (Working report No. 94/4), Allgemeine Reihe. ETH Zürich, Professur für Forstpolitik und Forstökonomie, Zurich, Switzerland.

BMLFUW (Ed.), 2008…2016. Holzeinschlagsmeldung. Federal Ministry for Agriculture, Forestry, Environment and Water Management, Vienna, Austria.

BMLFUW (Ed.), 2017. Austrian Green Report 2017, 58th ed. Federal Ministry for Agriculture, Forestry, Environment and Water Management, Vienna, Austria.

BMLFUW (Ed.), 2016. Austrian Green Report 2016, 57th ed. Federal Ministry for Agriculture, Forestry, Environment and Water Management, Vienna, Austria.

BMLRT (Ed.), 2020. Austrian Green Report 2020, 61st ed. Federal Ministry of Agriculture, Regions and Tourism, Vienna, Austria.

BMNT (Ed.) 2016…2018. Holzeinschlagsmeldung. Federal Ministry for Sustainability and Tourism, Vienna, Austria.

BMNT (Ed.), 2019. Austrian Green Report 2019, 60th ed. Federal Ministry for Sustainability and Tourism, Vienna, Austria.

BMNT (Ed.), 2018a. Einkommensermittlung für den Grünen Bericht – Description of the methodology version 2018. Federal Ministry for Sustainability and Tourism, Vienna, Austria.

BMNT (Ed.), 2018b. Austrian Green Report 2018, 59th ed. Federal Ministry for Sustainability and Tourism, Vienna, Austria.

Brandl, H., 2011. Experiences in Collecting Data on Farm Forest Enterprises over more than three decades. Small-scale Forestry 10, 135–147. https://doi.org/10.1007/s11842-011-9158-y

CEPF, n.d. The Confederation of European Forest Owners [WWW Document]. The voice of European forest owners. URL https://www.cepf-eu.org/page/cepf-1 (accessed 1.17.21).

Conti, G., Fagarazzi, L., 2005. Forest expansion in mountain ecosystems: “environmentalist’s dream” or societal nightmare? Planum 11, 1–20.

Darnhofer, I., 2014. Resilience and why it matters for farm management. European Review of Agricultural Economics 41, 461–484. https://doi.org/10.1093/erae/jbu012

Darnhofer, I., 2010. Strategies of family farms to strengthen their resilience. Environmental policy and governance 20, 212–222.

Darnhofer, I., Lamine, C., Strauss, A., Navarrete, M., 2016. The resilience of family farms: Towards a relational approach. Journal of Rural Studies 44, 111–122. https://doi.org/10.1016/j.jrurstud.2016.01.013

Dög, M., Wildberg, J., Möhring, B., 2018. Analysis of a long-term Forest Accountancy Network to Support Management and Controlling. Open Agriculture 3, 155–162. https://doi.org/10.1515/opag-2018-0016

Dupont, S., Pivato, D., Brunet, Y., 2015. Wind damage propagation in forests. Agricultural and Forest Meteorology 214–215, 243–251. https://doi.org/10.1016/j.agrformet.2015.07.010

EC, 2018a. EU Farm Economics Overview based on 2015 (and 2016) FADN data. European Commission, DG Agriculture & Rural Development, Brussels, Belgium.

EC, 2018b. Farm Accountancy Data Network – An A to Z of methodology.

EC, 2013. Concept of FADN [WWW Document]. European Commission - Agriculture and Rural Development. URL https://ec.europa.eu/agriculture/rica/concept_en.cfm (accessed 10.13.20).

EFI, 2020. Science Insights to the European Green Deal and Forests – Webinar, 20 May 2020.

Eurostat, 2017. Eurostat – Statistics explained [WWW Document]. Archive: Forestry statistics. URL https://ec.europa.eu/eurostat/statistics-explained/index.php/Archive:Forestry_statistics (accessed 1.17.21).

EUROSTAT (Ed.), 2000. Manual on economic accounts for agriculture and forestry EAA/EAF 97 (Rev. 1.1). Office for Official Publications of the European Communities, Luxembourg.

Evans, N., Llbery, B., 1993. The pluriactivity, part-time farming, and farm diversification debate. Environment and Planning A 25, 945–959.

FAOSTAT, 2020. Selected Indicators for Europe [WWW Document]. FAO Statistics Division. URL faostat.fao.org/static/syb/syb_5400.pdf (accessed 1.17.21).

Gardiner, B., Schuck, A., Schelhaas, M.J., Orazio, C., Blennow, K., Nicoll, B. (Eds.), 2013. Living with storm damage to forests, What Science Can Tell Us. European Forest Institute, Joensuu, Finland.

Gazzarin, C., Lips, M., 2018. Gemeinkostenzuteilung in der landwirtschaftlichen Betriebszweigabrechnung – eine methodische Übersicht und neue Ansätze. Austrian Journal of Agricultural Economics and Rural Studies 27, 9–15. https://doi.org/10.15203/OEGA_27.3

Hartebrodt, C., Hercher, W., 2012. Unde venis – quo vadis TBN von Fortran bis zum Bayes-Netz, in: Erklärungsmuster Im Flickenteppich – Ein Kaleidoskopischer Einblick in Die Privatwaldforschung Im Jahr 2012, Freiburger Forstliche Forschung – Berichte. Eigenverlag der FVA, Freiburg im Breisgau, pp. 1–18.

Hetemäki, L., 2020. The Green Deal and the EU Forest Sector.

Hoffmann, C., Stiefenhofer, A., Streifeneder, T., Hoffmann, C., Stiefenhofer, A., Streifeneder, T., 2010. The agro- structural change in the Alps and its outlook until 2020. A model based on key determinants. Presented at the European Association of Agricultural Economists, 118th Seminar, Unknown, Ljubljana, Slovenia. https://doi.org/10.22004/AG.ECON.95316

Hogl, K., Pregernig, M., Weiss, G., 2005. What is new about new forest owners? A typology of private forest ownership in Austria. Small-scale Forestry 4, 325–342. https://doi.org/10.1007/s11842-005-0020-y

Hyder, A., Lönnstedt, L., Penttinen, M., 1999. Accounting as a management tool for non-industrial private forestry. Scandinavian Journal of Management 15, 173–191.

Hyttinen, P., Huovinen, J., 1998. Synergy between Agriculture and Forestry at a farm level in Finland, in: Accounting and Managerial Economics for an Environmentally-Friendly Forestry. Presented at the International IUFRO Symposium, Institut national de la recherche agronomique, Nancy, France, pp. 355–363.

Hyttinen, P., Kallio, T., 1998. Sampling schemes for monitoring the socio-economics of farm forestry, EFI Proceedings. European Forest Institute, Joensuu, Finland.

Hyttinen, P., Niskanen, A., Ottitsch, A., 2000. New challenges for the forest sector to contribute to rural development in Europe. Land Use Policy 17, 221–232. https://doi.org/10.1016/S0264-8377(00)00014-4

Jilch, M., Kaluza, P., 2011. Die Landwirtepauschalierung für die Jahre 2011 bis 2015. SWK - Steuer- und Wirtschaftskartei 86, 71–75.

Jöbstl, H.A., 2000. Kosten- und Leistungsrechnung in Forstbetrieben - Betriebsabrechnung für die Praxis, Schriften aus dem Institut für Sozioökonomik der Forst- und Holzwirtschaft. Kommsionsverlag Österreichischer Agrarverlag, Wien.

Kirner, L., Fensl, F., Glawischnig, G., Hunger, F., 2020. Evaluierungsprojekt Wirtschaftlichkeit der Diversifizierung in Österreich. HAUP, LBG, LK OÖ, Vienna, Austria.

Kulakowski, D., Seidl, R., Holeksa, J., Kuuluvainen, T., Nagel, T.A., Panayotov, M., Svoboda, M., Thorn, S., Vacchiano, G., Whitlock, C., Wohlgemuth, T., Bebi, P., 2017. A walk on the wild side: Disturbance dynamics and the conservation and management of European mountain forest ecosystems. Forest Ecology and Management 388, 120–131. https://doi.org/10.1016/j.foreco.2016.07.037

Labarthe, P., Laurent, C., 2013. Privatization of agricultural extension services in the EU: Towards a lack of adequate knowledge for small-scale farms? Food Policy 38, 240–252. https://doi.org/10.1016/j.foodpol.2012.10.005

Lawrence, A., 2018. Do interventions to mobilize wood lead to wood mobilization? A critical review of the links between policy aims and private forest owners’ behaviour. Forestry: An International Journal of Forest Research 91, 401–418. https://doi.org/10.1093/forestry/cpy017

Lips, M., Schmid, D., 2013. Agrarische Diversifikation aus ökonomischer Sicht: Entwicklung auf den schweizerischen Landwirtschaftsbetrieben, in: Norer, R. (Ed.), Agrarische Diversifikation- rechtliche Aspekte von Agrotourismus bis Energieerzeugung, Tagungsband der 3. Luzerner Agrarrechtstagung 2012. Dike Verlag, Zürich, Switzerland, pp. 19–29.

MacDonald, D., Crabtree, J.R., Wiesinger, G., Dax, T., Stamou, N., Fleury, P., Gutierrez Lazpita, J., Gibon, A., 2000. Agricultural abandonment in mountain areas of Europe: Environmental consequences and policy response. Journal of Environmental Management 59, 47–69. https://doi.org/10.1006/jema.1999.0335

Mantau, U., Merlo, M., Sekot, W., Welcker, B., 2001. Recreational and environmental markets for forest enterprises: a new approach towards marketability of public goods. CABI Pub, Wallingford, Oxon, UK; New York.

Marongiu, S., Cesaro, L., Florian, D., Tarasconi, L., 2012. The use of FADN accounting system to measure the profitability of forestry sector. L’Italia Forestale e Montana 67, 253–261. https://doi.org/10.4129/ifm.2012.3.03

McNamara, K.T., Weiss, C.R., 2005. Farm Household Income and On-and-Off Farm Diversification. https://doi.org/10.22004/AG.ECON.43711

Mutenthaler, D., Sekot, W., 2016. A framework for explicit risk management in Austrian forest enterprises. Austrian Journal of Forest Science 133, 19–46.

Navarro, L.M., Pereira, H.M., 2015. Rewilding abandoned landscapes in Europe, in: Pereira, H.M., Navarro, L.M. (Eds.), Rewilding European Landscapes. Springer International Publishing, Cham Heidelberg New York Dordrecht London, pp. 3–23. https://doi.org/10.1007/978-3-319-12039-3

Niedermayr, J., Hoffmann, C., Stawinoga, A., Streifeneder, T., 2015. Agro-structural patterns in the Alps 2000–2010. Jahrbuch der Österreichischen Gesellschaft für Agrarökonomie 24, 275–284.

Niskanen, A., Sekot, W. (Eds.), 2001. Guidelines for Establishing Farm Forestry Accountancy Networks: MOSEFA, European Forest Institute research report. Brill, Leiden, Boston, Köln.

OECD, 2013. Household income, in: OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth. OECD Publishing, Paris, France, pp. 79–99.

Oesten, G., Roeder, A., 2012a. Management von Forstbetrieben – Band I, Grundlagen, Betriebspolitik, 3., überarbeitete Auflage. ed. Institut für Forstökonomie der Universität Freiburg, Freiburg, Germany.

Oesten, G., Roeder, A., 2012b. Management von Forstbetrieben – Band III, Leistungssystem, Zusammenfassung und Ausblick, 1. Auflage. ed. Institut für Forstökonomie der Universität Freiburg, Freiburg, Germany.

Peck, T., Korotkov, A., 1991. FAO/ECE forest resource assessment (temperate-zone) 1990, in: Forest Inventories in Europe with Special Reference to Statistical Methods: IUFRO Symposium, May 14-16, 1990, Birmensdorf, Switzerland/Edited by Michael Kohl, Dieter R. Pelz. Swiss Federal Institute for Forest, Snow, Birmensdorf, Switzerland.

Penttinen, M., Hakkarainen, J., 1998. Ratio Analysis Recommendations for Non-Industrial Private Forest Owners, Proceedings of the University of Vaasa. University of Vaasa, Vaasa, Finnland.

Rey Benayas, J., 2007. Abandonment of agricultural land: an overview of drivers and consequences. CAB Reviews 2. https://doi.org/10.1079/PAVSNNR20072057

Schmithüsen, F., Hirsch, F., 2010. Private forest ownership in Europe. Geneva timber and forest study paper 26.

Secco, L., Favero, M., Masiero, M., Pettenella, D.M., 2017. Failures of political decentralization in promoting network governance in the forest sector: observations from Italy. Land Use Policy 62, 79–100.

Sekot, W., 2017. Forest Accountancy Data Networks as a Means for Investigating Small-Scale Forestry: A European Perspective. Small-scale Forestry 16, 435–449. https://doi.org/10.1007/s11842-017-9371-4

Sekot, W., 2011. Assessing the sustainability of small scale forestry in Austria by means of regional levels of allowable cut. Austrian Journal of Forest Science 128, 195–218.

Sekot, W., 2007a. Stichprobendynamik als methodisches Problem von Testbetriebsnetzen, in: Fakultät für Forst- und Umweltwissenschaften der Universität Freiburg, Forstliche Forschungs- und Versuchsanstalt Baden-Württemberg (Eds.), Wald-Besitz-Ökonomie-2007, Freiburger Forstliche Forschung – Berichte. Eigenverlag der FVA, Freiburg i. Br., Germany, pp. 41–52.

Sekot, W., 2007b. European forest accounting: general concepts and Austrian experiences. Eur J Forest Res 126, 481–494. https://doi.org/10.1007/s10342-007-0170-x

Sekot, W., 2001. Analysis of profitability of small scale farm forestry (SSFF) by means of a forest accountancy data network – Austrian experiences and results, in: Niskanen, A., Väyrynen, J. (Eds.), Economic Sustainability of Small-Scale Forestry. EFI Proceedings Nr. 36. EFI. Joensuu, pp. 215–226.

Sekot, W., Toscani, P., 2020. Betriebszweigabrechnung für die Beratung von Forstbetrieben. AFZ – Der Wald 75, 27–29.

Sekot, W., Toscani, P., Karisch-Gierer, D., 2017. Betriebsvergleiche im österreichischen Kleinwald. AFZ – Der Wald 72, 42–44.

Sinabell, F., 2013. Das Einkommen in der Land- und Forstwirtschaft aus einem neuen Blickwinkel – Ergebnisse von Haushaltsbefragungen. Ländlicher Raum 03, 1–14.

Sinabell, F., Bock-Schappelwein, J., Firgo, M., Friesenbichler, K.S., Piribauer, P., Streicher, G., Gerner, L., Kirchner, M., Kantelhardt, J., Niedermayr, A., Schmid, E., Schönhart, M., Mayer, C., 2019. Eine Zwischenbilanz zu den Wirkungen des Programms der Ländlichen Entwicklung 2014-2020. Österreichisches Institut für Wirtschaftsforschung, Vienna, Austria.

Speidel, G., 1984. Forstliche Betriebswirtschaftslehre. Parey, Hamburg.

Stampfer, K., Dürrstein, H., Moser, A., 2001. Small-scale forestry challenges in Austria, in: Niskanen, A., Väyrnen, J. (Eds.), Economic Sustainability of Small-Scale Forestry, EFI Proceedings. European Forest Institute, Joensuu, Finland, pp. 177–184.

Statistik Austria (Ed.), 2020. Forstwirtschaftliche Gesamtrechnung - Methodische Hinweise. self-published, Vienna, Austria.

Statistik Austria, 2019. Standard-Dokumentation Metainformationen (Definitionen, Erläuterungen, Methoden, Qualität) zur Landwirtschaftlichen Gesamtrechnung (LGR) für Österreich. self-published, Vienna, Austria.

Streifeneder, T., 2010. Die Agrarstrukturen in den Alpen und ihre Entwicklung unter Berücksichtigung ihrer Bestimmungsgründe: Eine alpenweite Untersuchung anhand von Gemeindedaten. Herbert Utz Verlag.

Streifeneder, T., Tappeiner, U., Ruffini, F.V., Tappeiner, G., Hoffmann, C., 2007. Selected Aspects of Agro-structural Change within the Alps: A Comparison of Harmonised Agro-structural Indicators on a Municipal Level in the Alpine Convention Area. rga 41–52. https://doi.org/10.4000/rga.295

Toscani, P., Sekot, W., 2018. Forest Accountancy Data Networks – A European Approach of Empirical Research, Its Achievements, and Potentials in Regard to Sustainable Multiple Use Forestry. Forests 9, 220. https://doi.org/10.3390/f9040220

Toscani, P., Sekot, W., 2017. Assessing the Economic Situation of Small-Scale Farm Forestry in Mountain Regions: A Case Study in Austria. Mountain Research and Development 37, 271–280. https://doi.org/10.1659/MRD-JOURNAL-D-16-00106.1

Toscani, P., Sekot, W., 2015. Assessing the Economy of Small Scale Farm Forestry at The National Scale: The Case of Austria. Small-scale Forestry 14, 255–272. https://doi.org/10.1007/s11842-015-9286-x

Toscani, P., Sekot, W., 2014. Modellierung einer forstlichen Betriebszweigabrechnung für freiwillig buchführende Betriebe [Modelling full cost accounting for the forestry part of farms with voluntary book-keeping], in: Hambrusch, J., Kantelhardt, J., Oedl-Wieser, T., Stern, T. (Eds.), Jahrbuch Der Österreichischen Gesellschaft Für Agrarökonomie. facultas, Institut für Agrar- und Forstökonomie, Universität für Bodenkultur Wien, Feistmantelstraße 4, Wien, Austria, pp. 79–88.

Toscani, P., Sekot, W., Hoffmann, C., Dellantonio, S., 2018. Aufbau eines Testbetriebsnetzes im Kleinwald Südtirols. AFZ – Der Wald 38–40.

UNECE, CES (Eds.), 2011. Canberra Group – Handbook on Household Income Statistics, 2nd edition. ed. United Nations Economic Commission for Europe, New York and Geneva.

Urban, C., 2011. Die neue land- und forstwirtschaftliche Pauschalierungsverordnung 2011. FJ - Finanzjournal 51, 71–75.

van Zonneveld, M., Turmel, M.-S., Hellin, J., 2020. Decision-Making to Diversify Farm Systems for Climate Change Adaptation. Front. Sustain. Food Syst. 4, 32. https://doi.org/10.3389/fsufs.2020.00032

Weiss, G., Lawrence, A., Hujala, T., Lidestav, G., Nichiforel, L., Nybakk, E., Quiroga, S., Sarvašova, Z., Suarez, C., Živojinović, I., 2019. Forest ownership changes in Europe: State of knowledge and conceptual Foundations. Forest Policy and Economics 99, 9–20.

Weltin, M., Zasada, I., Franke, C., Piorr, A., Raggi, M., Viaggi, D., 2017. Analysing behavioural differences of farm households: An example of income diversification strategies based on European farm survey data. Land Use Policy 62, 172–184.