Schlüsselbegriffe: Bodenerwartungswert, Kapitalwert, Europäische Buche, Sturmschäden, Preisunsicherheit, Sicherheitsäquivalent, Monte-Carlo-Simulation

Available at https://doi.org/10.53203/fs.2601.1

See below the issue 1/2026 as E-Paper or have a look at our E-Paper archive dating back to 1955.

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

Abstract

This study presents a targeted literature review of three forest economic models within the Faustmann tradition under conditions of natural risk, with an emphasis on Fagus sylvatica forests. It evaluates different ways of incorporating risks such as storms, insect outbreaks, and timber price volatility. The comparison is based on methods for estimating Land Expectation Value (LEV) or Net Present Value (NPV), on the stochastic approaches adopted, and on the handling of uncertainty. Methodologically, a targeted Scopus review identified three Faustmann-related risk models applied to Fagus sylvatica from 2001 to 2014. The LEV/NPV formulations are reconstructed and a structured comparison of risk integration, assumptions, and model design is executed. Particular emphasis is placed on the ecological and economic characteristics of Fagus sylvatica and on the challenges of its management in a changing environment. Overall, the increased vulnerability of Fagus sylvatica to natural hazards makes models that incorporate its biological particularities necessary, while among the approaches examined, the Poisson-type stochastic storm framework with age/height-dependent damage emerges as the most suitable in terms of realism and validity.

Zusammenfassung

Diese Studie präsentiert eine gezielte Literaturübersicht zu drei forstökonomischen Modellen in der Faustmann-Tradition unter Bedingungen natürlicher Risiken, mit Schwerpunkt auf Wäldern von Fagus sylvatica. Sie bewertet verschiedene Ansätze zur Einbeziehung von Risiken wie Stürmen, Insektenkalamitäten und Schwankungen der Holzpreise. Der Vergleich basiert auf den Methoden zur Schätzung des Land Expectation Value (LEV) beziehungsweise des Net Present Value (NPV), auf den verwendeten stochastischen Ansätzen sowie auf dem Umgang mit Unsicherheit. Methodisch wurden im Rahmen einer gezielten Scopus-Recherche drei Faustmann-bezogene Risikomodelle identifiziert, die im Zeitraum 2001 bis 2014 auf Fagus sylvatica angewendet wurden. Die LEV/NPV-Formulierungen werden rekonstruiert und ein strukturierter Vergleich der Risikointegration, der Annahmen und der Modellgestaltung vorgenommen. Besonderes Augenmerk gilt den ökologischen und ökonomischen Eigenschaften von Fagus sylvatica sowie den Herausforderungen ihrer Bewirtschaftung in einem sich wandelnden Umfeld. Insgesamt macht die erhöhte Anfälligkeit von Fagus sylvatica gegenüber Naturgefahren Modelle erforderlich, die ihre biologischen Besonderheiten explizit berücksichtigen, wobei sich unter den untersuchten Ansätzen der stochastische Sturmrahmen vom Poisson-Typ mit alters- und höhenabhängigem Schaden als der hinsichtlich Realismus und Validität geeignetste erweist.

1 Introduction

Calculating the value of forest land constitutes a basic pillar of Forest Economics. Investment in the management of a forest has the particular feature that it requires significantly more capital per unit of output than almost any other economic venture (Binkley, 1993). In addition, it is characterised by long-term planning, complex interdependencies between economic and ecosystem factors, and substantial exposure to uncertainty. For this reason, any economic theory mobilised to estimate the value of such an investment is called upon, beyond the basic quantities of economic evaluation, to incorporate those factors and parameters that capture the risk inherent in timber production as a commercial product of biological origin, such as losses from fires, windthrow, frosts and insect attacks.

The now classic Faustmann forest economic model (Faustmann, 1849) has for decades formed the basis of forest economic theory, providing a way to determine the Land Expectation Value (LEV) (Papaspyropoulos & Karamanolis, 2018; Mpekiri & Papaspyropoulos 2026) and the economically optimal rotation period, that is, the one that maximises LEV (Optimal Rotation Period) over perpetual cycles of stand regeneration. However, this model rests on highly restrictive assumptions: complete certainty with respect to timber prices, the interest rate, stand growth and patterns of natural disturbances (Klemperer, 1996; Tahvonen & Viitala, 2006). In practice, however, forest managers operate in a dynamic environment shaped by market volatility and an ever-increasing exposure to natural hazards such as storms, fires and insects — factors that are particularly relevant in the context of climate change (Loisel, 2014; Rakotoarison & Loisel, 2017).

Fagus sylvatica is a dominant native broadleaved species in Europe (Bolte et al., 2007; Dittmar et al., 2003; Leuschner, 2020), estimated to cover over 11 million hectares (Antonucci et al., 2021). In Central Europe Fagus sylvatica is the most common (Ellenberg, 1996) and successful tree species (Leuschner et al., 2006), owing much of its prolific presence to its highly competitive nature (Ellenberg, 1996; Leuschner, 2020) in site conditions of moderate moisture and acidity that prevail across much of this region (Bolte et al., 2007). It is described as a shade-tolerant species that exhibits high success in older ages and displays high competitiveness, often preventing the establishment of other tree species beneath the dominant beech canopy (Antonucci et al., 2021). Due to its high shade tolerance, Fagus sylvatica is well adapted to silvicultural systems that maintain canopy cover (Uhl et al., 2025). Across Europe, shelterwood and continuous-cover or selection based systems are recommended for Fagus sylvatica and converted coppices (Fuchs et al., 2025; Nocentini, 2009; Spanos et al., 2021), while minimal intervention or even abandonment might be the optimal strategy especially in terms of biodiversity conservation and carbon sequestration (Markuljaková et al., 2025).

At the same time, Fagus sylvatica is sufficiently resilient to grow even in less favorable site conditions, ranging from moderately dry locations to periodically wet soils (Antonucci et al., 2021) due to its genotypic and phenotypic flexibility (Roibu et al., 2022). Consequently, its distribution extends across almost the whole of Europe, from the Atlantic regions of Western Europe (Antonucci et al., 2021) and many western countries such as Germany, France and the Netherlands (Hanewinkel et al., 2013), to the continental climates of Central Europe and even the Mediterranean zone of Southern Europe (Antonucci et al., 2021). In terms of altitude, in Central Europe Fagus sylvatica can be found in the low-elevation lowlands that constitute its forest mosaic (Antonucci et al., 2021), at altitudes as low as 100-900 m (a.s.l.) (Fuchs et al., 2025). In Italy, Fagus sylvatica forests (Fagus sylvatica L.) form a characteristic component of many mountain landscapes, from the Alps (forming pure stands above 1000 m) to the southern regions of Campania, Basilicata, Calabria and Sicily in the Mediterranean zone where it can descent to altitudes as low as 400-500 m under high air moisture conditions (Nocentini, 2009). In Greece, Fagus sylvatica occurs at high elevations, mainly in the mountainous zones of Pindos and Rhodope, and its altitudes can reach between 700 and 1800 m. (Spanos et al., 2021). Finally, a closely related species, Fagus sylvatica subsp. orientalis is also frequently found in in Central and Southeastern Europe, in regions such as Greece (Spanos et al., 2021) and Turkey (Fuchs et al., 2025), and while its responses to climate change are not identical to Fagus sylvatica, it can be argued that they have enough similarities (Fuchs et al., 2025) that similar management strategies and forest economic models could be applied to both of them.

Despite its natural resilience, Fagus sylvatica faces many challenges, especially in light of climate change (Antonucci et al., 2021; Leuschner, 2020). As a species it is particularly vulnerable to storm damage because of its shallow root system and large crown surface area (Bolte et al., 2007; Houston Durrant et al., 2016). It is also prone to spring frosts, which destroy young leaves, as well as to fires due to its thin bark (Houston Durrant et al., 2016). Although shade-tolerant and resistant to low temperatures, it is vulnerable to prolonged periods of drought (Geßler et al., 2006; Jump et al., 2006; Leuschner, 2020; Lindner et al., 2010; Martinez Del Castillo et al., 2022; Sperlich et al., 2024) and to early frost that destroys its new leaves and flowers (Houston Durrant et al., 2016). Climate change also affects the growth rate of Fagus sylvatica stands, which is estimated to be reduced by approximately 20% to as much as 50% in various European regions (Martinez Del Castillo et al., 2022). A frequently cited reason for that is the increased and prolonged droughts that come as a result of changing climate conditions, such as the expected rise in temperature while precipitation remains constant (Geßler et al., 2006; Jump et al., 2006; Spanos et al., 2021). At the same time, for forest ecosystems change due to climate change is predominantly driven by large-scale extreme events (Hanewinkel, Peltola et al., 2010) such as storms and wildfires. Additionally, temperature rises, precipitation changes, and the ever increasing appearance of abiotic disturbances such as storms and long droughts, are frequently associated with biotic risks such as outbreaks of pests and diseases (Liepiņš & Bleive, 2025). In Greece, for example, Fagus sylvatica faces risks from root-rot fungi, overgrazing and climate change (Spanos et al., 2021). Another pest that is frequently associated with drought and widespread in Fagus sylvatica populations in Central and Eastern Europe regions (Holuša et al., 2025; Špoula et al., 2024) as well as South Europe (Vujanovic et al., 2020) is the beech bark beetle (Taphrorychus bicolor).

However, Fagus sylvatica is not the only European species experiencing the adverse effects of climate change. Picea abies, which until recently outnumbered Fagus sylvatica and was preferred by foresters (Geßler et al., 2006), is described as “one of the big ‘losers’ of climate change” (Hanewinkel, Hummel et al., 2010). In the past, conifer species, such as Picea abies or Pinus sylvestris (Girona-García et al., 2018), had been introduced into Fagus sylvatica forests, or even completely replaced them due to high demands in firewood for coal (Liepiņš & Bleive, 2025; Övergaard & Stener, 2010). However, Fagus sylvatica represents the natural forest vegetation species across wide areas of Central and Western Europe (Antonucci et al., 2021), and even on more humid sides in the mountain ranges of Southern Europe (Kermavnar et al., 2023; Nocentini, 2009).

Furthermore, compared to other species, Fagus sylvatica has the advantage of being better equipped to preserve the forest climate and preserve important ecological functions (biochemical cycling, biodiversity) (Tarp et al., 2000). As a result, we see a recent trend in European forest policy where Fagus sylvatica is increasingly mixed into coniferous monocultures (Geßler et al., 2006; Moosmayer, 2002) as well as natural expansion into neighboring conifer stands (Nocentini, 2009). In central Europe, the transformation of Picea abies forests into Fagus sylvatica forests is taking place on a large scale (Spiecker et al., 2004). Additionally, altitudinal migrations of Fagus sylvatica have also been recorded (Nocentini, 2009; Peñuelas & Boada, 2003).

These ongoing changes, either gradual or large-scale due to massive destructive events, beg the question of how they can be evaluated in economic terms and what, if any, conclusions can be drawn regarding the management of Fagus sylvatica in Europe, since the economic impact of disturbances is particularly pronounced in managed forests (Zeng et al., 2009). For example, in Austrian forests, salvage logging accounted for 39% of total timber harvests during 2006–2023 from both biotic (such as bark beetle) and abiotic (for example storms and wind breaks) causes (Schwarzbauer et al., 2025). At the same time, the economic importance of Fagus sylvatica and other European species has declined in recent decades due to high production costs (Brazee & Newman, 1999), decreasing timber prices and structural transformations in the wood-processing industry (Rakotoarison & Loisel, 2017). These developments make it imperative to revise management strategies for Fagus sylvatica forests under risk conditions and, consequently, to propose forest economic models adapted to the specific characteristics and needs of this valuable species.

Over the last two decades, various extensions of the Faustmann model have been proposed to take these risks facing Fagus sylvatica into account. Reed (1984) incorporated fire risk in a continuous-time framework, showing that under certain conditions the risk can be incorporated through an adjustment of the discount rate. However, this simplification fails when damages depend endogenously on stand structure or when price uncertainty is dependent on the historical path of prices. In response, more recent studies have incorporated stochastic elements, such as storm arrival modelled as a Poisson process, price volatility (via autoregressive or Brownian models) and flexible harvesting strategies (such as the minimum acceptable price strategy), in order to better reflect the complex decision-making problem in production forests (Knoke & Wurm, 2006; Loisel, 2014).

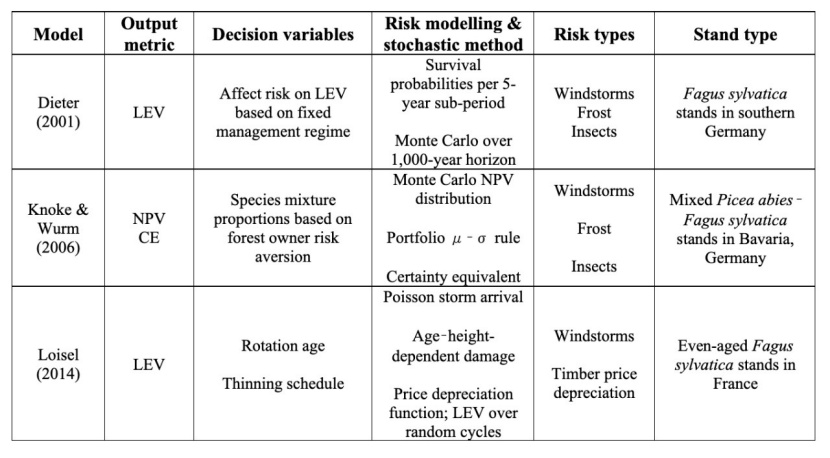

The present study focuses on three key forest economic models in the Faustmann tradition that incorporate various types of risk relevant to Fagus sylvatica:

i. Risk from windstorms, insect damage and frost in Fagus sylvatica (Dieter, 2001).

ii. Risk from windstorms, insect damage and frost in mixed Picea abies-Fagus sylvatica forests (Knoke & Wurm, 2006).

iii. Windstorms and timber price risk applied to an even-aged beech stand (Loisel, 2014).

Ιn what follows, the term “Faustmann framework” is used in a broad sense to include both explicit extensions of the classical LEV model (Dieter, 2001; Loisel, 2014) and closely related discounted NPV approaches developed in the same tradition (Knoke & Wurm, 2006), insofar as they address the valuation of forest land and timber under risk. The aim is to provide a concise presentation and comparison of these extensions of the Faustmann model, with particular emphasis on their applicability to the management of Fagus sylvatica, through the examination of the application of these models to both pure and mixed Fagus sylvatica stands by Dieter (2001), Knoke and Wurm (2006) and Loisel (2014). The paper discusses both the methodological assumptions and the implications for forest policy regarding the incorporation of different types of risk into the planning of harvests and thinnings. Given the increasing instability of natural and economic systems in view of climate change, proposing new theoretical extensions and adaptation practices for both the economic and ecological management of production forests is a challenge for the science of Forest Economics.

2 Materials and Methods

For the selection of the studies under examination, a targeted literature review was carried out using data drawn from the Scopus database. Initially, a search was conducted in Scopus for all available articles with the term “Faustmann” in the title, abstract or keywords (Mpekiri & Papaspyropoulos, 2026). Focusing on the terms “risk”, “storm risk” and “fire risk”, the scientific articles were identified that were related to extensions and modifications of the Faustmann framework dealing with risk from windthrow, storms, fires, frost and insect attacks. Subsequently, articles referring to tree species that do not frequently occur in Europe or have no known commercial importance in the European forest sector, such as Pinus taeda, Pinus radiata and Picea sitchensis, were excluded. Among the species that are found in Europe, Pinus pinaster has mainly coastal distribution and limited management for timber production, whereas Fagus sylvatica is a species with significant distribution in the high forests of Central Europe (Leuschner, 2020) as well as Southern regions such as Italy (Nocentini, 2009), Spain (Peñuelas & Boada, 2003) and Greece, and with a valuable timber-producing character (Spanos et al., 2021). In addition, it is known to be vulnerable to natural disturbances such as storms, frosts and fires (Bolte et al., 2007; Houston Durrant et al., 2016), which makes it a particularly relevant species for studies of forest economic risk. The final sample comprises three studies covering the period 2001–2014. Two of them (Dieter, 2001; Loisel, 2014) extend the classical Faustmann LEV model by incorporating various types of risk, while the third (Knoke & Wurm, 2006) analyses risk and return in mixed Picea abies-Fagus sylvatica stands using an NPV-based portfolio approach. The inclusion of Knoke and Wurm (2006) is further motivated by current European policy trends to increase the share of Fagus sylvatica in conifer-dominated stands to enhance resilience.

From the three selected studies, we extracted the mathematical formulations used to calculate the Land Expectation Value (LEV) or the Net Present Value (NPV) and, where applicable, the economically optimal rotation period; in Dieter (2001) and Loisel (2014) these correspond to explicit risk-extended versions of the classical Faustmann model, whereas in Knoke and Wurm (2006) they are part of an NPV-based portfolio framework. Then, for each model, the individual variables and parameters that constitute it were analysed. Finally, a comparative assessment of the three models was carried out. The comparison of the models took place on the basis of:

i) their theoretical approach,

ii) their basic assumptions about forest structure and growth,

iii) the types of risk they cover and the method of incorporating it, and

iv) their applicability to Fagus sylvatica under the constantly evolving conditions of climate change that affect European forestry.

3 Results

3.1 The model of Dieter (2001)

The model of Dieter (2001) employs a mathematical expression of LEV based on the work of Samuelson (1976) and Pertz (1983), in which the classical assumptions of the Faustmann model are adopted, such as constant stand growth, uniform silvicultural practices, fixed harvesting age and roundwood prices, and identical costs and interest rates throughout the time horizon. The Faustmann mathematical model used by Dieter is given below in Equation (1):

Where B0 is the Land Expectation Value, Au is the yield at the end of the rotation period, u is the length of the rotation period, Da is the intermediate yields from thinnings at age a, i is the interest rate, c is the establishment or reforestation cost and V is administrative costs.

The key innovation of the model is the incorporation of survival probabilities, which take into account the probability tn that the stand survives during the transition from sub-period n to n+1 and the total survival probability sj up to age j, as the product of the transitions, which is given by Equation (2):

These probabilities are derived from empirical mortality data related to the effects of storms and insects. In the study, the probability that a Fagus sylvatica stand reaches age 140 years is 97%, compared with only 86% for other forest species such as Picea abies, a fact that is attributed to the greater stability of Fagus sylvatica at older ages.

Subsequently, the effect of the risk due to storm damage or insect attack on LEV is calculated by simulation using the Monte Carlo method, where the following are simulated: 1.000 iteration per rotation (80–140 years), a time horizon of 1.000 years and random variables which determine every 5 years whether the stand survives or is destroyed.

In each iteration, if the stand survives up to u, it is harvested normally with revenue Au and intermediate thinnings Da. If the stand suffers damage at age j < u, then the yield is reduced by 50% (assuming a collapse in timber prices) and new planting is required (cost c = 2.500 €/ha). By contrast, if it reaches the end of the rotation without damage, natural regeneration costs only 1.500 €/ha. The discount rate is kept constant (2%).

The results of the simulations indicate that LEV decreases by only 2–5% in Fagus sylvatica stands (compared with 4-15% in Picea abies) under the influence of storm or insect risk, compared to the absence of risk. According to Dieter, this result arises as a direct consequence of the higher survival probability of Fagus sylvatica, especially at older stand ages, as shown in his survival curves. However, since Picea abies has higher LEV on the whole as a species compared to Fagus sylvatica, Dieter concludes that Picea abies is still preferrable to Fagus sylvatica, even in the presence of risk.

3.2 The model of Knoke and Wurm (2006)

Knoke and Wurm (2006) approached the issue of risk assessment by applying portfolio theory (Elton & Gruber, 1995) to evaluate trade-offs between risk and return in mixed Picea abies (Picea abies) and Fagus sylvatica stands with harvesting periods of 101–110 years for Picea abies and 121–130 years for Fagus sylvatica.

To calculate the proportion of damage from “natural hazards”, that is, risks from windthrow, insects and frost, they adjusted the Fagus sylvatica survival probability curves from one sub-period of the harvesting period to the next (Equation 2) of Dieter (2001), so as to predict more realistically the proportions of damaged wood volume. Among other findings, they observed that the sum of all salvage harvests due to natural risks for Fagus sylvatica corresponds to only 11% of the planned harvest (as opposed to more than 40% for Picea abies). They modelled timber price fluctuations using a regression model for Fagus sylvatica, based on price data from Bavaria, where Fagus sylvatica is extremely widespread.

For assessing the impact of risk on forest value, Knoke and Wurm (2006) relied on the Net Present Value (NPV) rather than LEV, in order to be able to adapt portfolio theory, which is based on the sum of discounted net revenue flows (Net Revenue Factors or NRF), to the needs of evaluating a forest investment. To calculate NPV in a mixed forest with two tree species (Fagus sylvatica and Picea abies) they used Equation (3):

Where α1 and α2 are the percentages of each tree species, with α1 + α2 = 1 (with an optimal mixture ~70% Fagus sylvatica, 30% Picea abies) and npv1 and npv2 are the Net present value of Picea abies and Fagus sylvatica respectively, calculated as the sum of all discounted net revenue flows (Net Revenue Factors or NRF)

Based on Equation (3), Knoke and Wurm (2006) used Monte Carlo simulations, in a similar way to Dieter (2001) (1,000 repetitions per rotation period, 1,000-year time horizon, under the assumption that if the stand is damaged before completion of the rotation period, its yield is reduced by 50%), to generate the distribution of NPV values and the Expected Net Present Value (E(NPV)).

They then calculated the standard deviation of the expected value of NPV, as obtained from the Monte Carlo simulations, as a way of quantifying financial risk (Pflaumer, 1992), using Equation (4) (Markowitz, 1952).

Where SNPV is the standard deviation of the NPV of a mixed forest with a given species composition, snpv1 and snpv2 are the standard deviations of the NPVs of the individual species, and knpv1,npv2 is the correlation coefficient between the net present values of the two species.

Finally, they used the μ–σ rule (mean–variance rule) to calculate the “risk” of the forest investment for the forest owner, expressed as the Certainty Equivalent (CE), in accordance with Markowitz’s (1952) portfolio theory, as shown in Equation (5):

Where CE is the Certainty Equivalent, E(NPV) is the Expected Net Present Value, S2NPV is the variance of financial returns and α is a constant that depends on the decision maker’s attitude towards risk.

The results of applying this model and the Monte Carlo simulations by Knoke and Wurm (2006) lead to the conclusion that the greater the forest owner’s aversion to risk, as expressed by the constant α, the higher the optimal proportion of Fagus sylvatica in forest stands. In their simulations, α ranges from 0.5 (almost no risk aversion) to 2.5 (very risk-averse). When risk is ignored and only expected NPV is considered, the optimal portfolio consists of pure Picea abies (0% Fagus sylvatica). As risk aversion increases, the optimal share of Fagus sylvatica rises and reaches about 60% for highly risk-averse decision-makers (α = 2.5).

3.3 The model of Loisel (2014)

Loisel (2014) developed a modification of Reed’s (1984) model with rigorous mathematical foundations, aiming to incorporate storm risk at stand level into LEV, as well as timber depreciation due to oversupply after a storm, in a direct and structural way, avoiding the usual approach of simply increasing the discount rate. The main components of Loisel’s (2014) model are as follows:

1. The temporal model of storm occurrence which is expressed by the cumulative probability density function (CDF) based on a Poisson process, and is given by Equation (6):

Where x is the time interval from the last storm (or start of the period) to the next one, λ is the mean number of storms per unit of time; it is the intensity of the Poisson process and F(x) is the probability that at least one storm will occur at time x.

2. The model of the effect of a storm on the forest, which depends on the age of the forest, related to tree height at the time of the storm, and is expressed by Equations (7) and (8):

Where H(t) is the tree height as a function of time, tL is the time at which the tree reaches the “critical” height HL, beyond which there is an increased risk of damage, and HL is the threshold height above which a storm can cause damage.

Where α(t) is the expected % of trees that survive at time t and θτ is the % of trees that are damaged if the storm occurs after the threshold τ > tL.

3. The model of timber depreciation, which is expressed by the timber price under risk (Equation 9) and by the depreciation as a function of the time since the storm (Equation 10):

Where pt is the current timber price at time t, under risk, p0 is the reference timber price, i.e. the price without storm risk and ρ𝜏𝑡−(t) is the percentage depreciation of the timber price at time t, which depends on the time elapsed since the last storm 𝜏𝑡−

Where ρ0 (.) is the baseline depreciation function, which depends only on the time elapsed since the last storm and t – 𝜏𝑡− is the time that has elapsed since the last storm.

4. The Faustmann Value (LEV), under the assumption that storms occur independently and randomly over time, is given by Equation (11):

Where δ is the discount rate, τ is the random duration of a cycle (due to storms or harvesting) and (y) is the expected net return of a cycle, which is given by Equation (12)

Where H(0, τi, σ) are the revenues from thinnings, taking into account past storms, V(θτ, ξτ, τi ) is the final revenue in the event of a storm, Cn(θτ, τi ) is the clearing cost (fixed cost c0 + variable cost proportional Cν proportional to the volume of damaged trees) and c1 is the reforestation cost.

On the basis of Equation (12) one may see that the main difference between Loisel’s (2014) model and Reed’s (1984) is that in the calculation of LEV the revenues from thinnings are included, which affect the final total income in the event of a storm. Therefore, even if the final revenue is lower due to damage, the intermediate revenues can make the overall return comparable to the case without storms.

Loisel’s (2014) model was applied to data from Fagus sylvatica forests in France, with a harvesting period of 100 years, and the results showed that storm risk substantially reduces the economically optimal rotation period.

4 Discussion

The three studies examined — Dieter (2001), Knoke and Wurm (2006) and Loisel (2014) — represent three different approaches rooted in or closely related to the classical Faustmann forest economic model, with the aim of incorporating risk into the economic valuation and management of production forests, particularly those dominated by Fagus sylvatica.

4.1 Windstorm, insect risk and frost damage in empirically based Faustmann LEV models (Dieter, 2001)

Dieter’s (2001) model, based on a mathematical formulation of the Faustmann model by Samuelson (1976) and Pertz (1983), constitutes an introductory approach to incorporating risk into the calculation of Land Expectation Value (LEV). His approach was methodologically based on incorporating survival probabilities of Fagus sylvatica stands into discrete subdivisions of the rotation period. These probabilities, however, were empirically derived from mortality data of Fagus sylvatica forests after insect attacks or the effects of storms in southern Germany, with a harvesting period for Fagus sylvatica of 140 years. This is of great importance for the subsequent conclusions drawn from the model, since the empirical survival probability distribution of Fagus sylvatica could lead to an underestimation of the impact of risk on LEV, as the resilience of Fagus sylvatica stands increases significantly at older ages. Indicatively, according to the model results, LEV in Fagus sylvatica stands decreases by only 2–5% due to storms or insects, which suggests that these risks may be underestimated in this methodological approach. Given the species’ vulnerability to windthrow because of its shallow root system, which is particularly pronounced at younger ages (Bolte et al., 2007; Houston Durrant et al., 2016), models that take into account stand age at the time when a storm or insect attack occurs might yield greater accuracy in risk estimation for production Fagus sylvatica forests. In this sense, Dieter’s formulation is useful as a first, practical step towards integrating natural risk, but it is dependent on the accuracy of empirical data and therefore it unknown whether it can be generalized to the entirety of Fagus sylvatica’s European distribution.

4.2 Windstorm, insect risk and frost damage in mixed beech–spruce portfolio investment models (Knoke & Wurm, 2006)

A different approach was offered by the model of Knoke and Wurm (2006). Recognizing the gaps in Dieter’s (2001) empirical estimation of Fagus sylvatica stand survival probabilities, they proposed a more realistic survival probability curve based on the empirical data used by Dieter (2001). Their approach, however, differed from Dieter’s in that they focused on Net Present Value (NPV) instead of LEV, relying on the μ–σ rule of portfolio theory (Elton & Gruber, 1995). This theoretical approach allows them to interpret the risk from natural disasters and biotic factors, which are a particular feature of forest management, as an investment prospect, as a form of financial risk, something that differs from the classical Faustmann approach. In this way, Knoke and Wurm (2006) manage to introduce into the Faustmann tradition the factor of forest owners’ attitude towards the risk of economic investment in the management of a Fagus sylvatica – Picea abies production forest. Furthermore, this shift towards a stochastic portfolio setting directly responds to criticisms that many bioeconomic forest models are overly simple — deterministic, single-species and largely ignoring risk and biological realism (Bulte & Van Kooten, 1999; Griess & Knoke, 2013; Knoke & Seifert, 2008). Thus, the model of Knoke and Wurm (2006) allows a fairly flexible harvesting policy, which is based on logging only when the economic rent is maximised and the anticipated risk is minimised. The findings of Knoke and Wurm (2006) indicate that the optimal proportion of Fagus sylvatica in the mixture increases in proportion to the forest owner’s aversion to risk. Their model, however, makes the assumption that each of the species in the mixed stand would grow identically to how they would in two pure stands. There is evidence that neighboring effects play an important role in the growth of individual species (Hanewinkel, Peltola et al., 2010; Leuschner, 2020; Nocentini, 2009). Lastly, Knoke and Wurm’s model is also dependent on empirical data for a specific region within the distribution of Fagus sylvatica. Due to this fact and it’s lack of mathematical formalism, it is difficult to generalize to more extended areas of the distribution of either Picea abies or Fagus sylvatica.

4.3 Windstorm and timber price risk in formal Faustmann-type models (Loisel, 2014)

Loisel’s (2014) model differs considerably from the two previous ones by Dieter (2001) and Knoke and Wurm (2006), as it constitutes a comprehensive and analytical mathematical approach, filling gaps and weaknesses of the two earlier models. It is a formalistic model, meaning it is not tied to any specific species, but focuses on the derivation of general mathematical formulas for modeling three aspects of risk integration: modeling storm risk, modeling the impact of a storm on the stand, and modeling the depreciation of timber prices following a destructive event. It introduces a stochastic Poisson methodology for calculating the timing of independently occuring storm events, which represents more faithfully the unpredictable behavior of climatic conditions, especially in the presence of climate change. In addition, the model allows specific adaptation to species with high vulnerability to damage from storms and windthrow, such as Fagus sylvatica, due to its shallow root system, since it incorporates tree height as a function of storm occurrence time into the model for calculating the expected net return of a cycle, a quantity that Knoke and Wurm (2006) associated with timber price and approximated using Monte Carlo simulations, which is a frequently used stochastic modeling tool in the integration of different types of risks in economic theory (Dieter, 2001; Knoke & Wurm, 2006; Kurz et al., 2008). The advantage of Loisel’s (2014) approach is that it links the probability of damage to the forest with a biological characteristic of the forest species, namely tree height as a function of age, and incorporates this quantity into the calculation of LEV. This gave their forest economic model the flexibility to be adapted to the needs of species vulnerable to windthrow and storm damage, such as Fagus sylvatica, by allowing thinning harvests to be scheduled earlier and thus reducing stand vulnerability in areas with high storm frequency. In this way, it simulates much more realistically the impact of storms on species such as Fagus sylvatica which becomes particularly resilient at older ages. Additionally, while both Dieter (2001) and Knoke and Wurm (2006) included revenues from planned thinnings without considering storm timing, Loisel’s model introduces revenues from thinnings in a mathematically rigorous way that takes into account timber prices adjusted based on the length of time since the previous storm. This is especially important for the applicability of the model to Fagus sylvatica under climate change, where storms appear in increasing frequency and selection-based sylvicultural systems are still widely used. Finally, Loisel (2014) provided a much more accurate and mathematically reliable method for calculating LEV, as he incorporated into the model the revenues from thinnings and the depreciation of timber after storm damage incidents due to the sharply increased supply of timber on the market. Despite its many advantages, this model has a few assumptions that can make it difficult to apply in specific circumstances. For example, the model adopts the assumption of (Schmidt et al., 2010) that storms have a small impact on young stands, and therefore assume that if a storm occurs before the critical time tL, there is no damage to the stand. While it is widely documented, as discussed previously in this paper, that Fagus sylvatica is in general much more resilient to destructive events than conifer species like Picea abies, it is vulnerable to windthrow at a young age and therefore an assumption such as this could potentially lead to an underestimation of the impact of storm. Lastly, storms are assumed to occur randomly and independent of one another. In the context of climate change, that is likely to differ, as climate change may cause an increase in the frequency and severity of storms in Europe (Loisel, 2014).

4.4 Synthesis across risk types and model assumptions

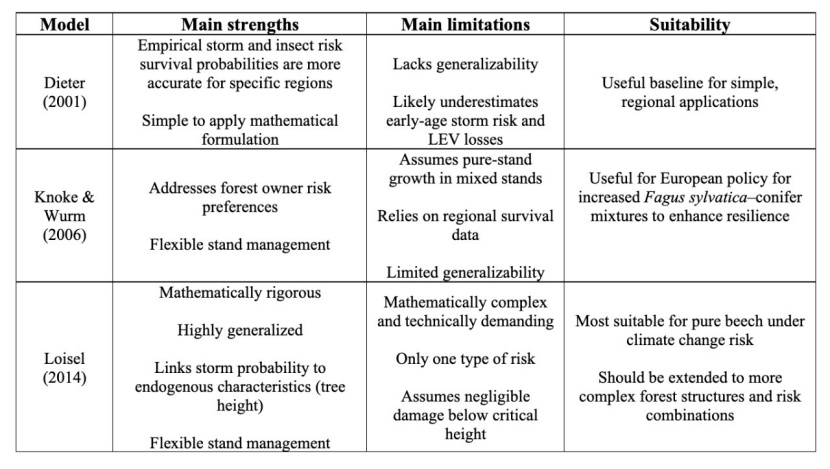

To synthesize the findings of the three reviewed models, we outline their basic assumptions (stand types, output metrics, decision variables, risk types and risk modeling methods) and their main advantages and disadvantages in two tables. Table 1 provides a concise overview of the assumptions that form the basis of each model, while Table 2 distils their main strengths, limitations and suitability of each model for Fagus sylvatica.

Table 1: Key assumptions of the Dieter (2001), Knoke and Wurm (2006) and Loisel (2014) forest economic models integrating natural risk for Fagus sylvatica.

Tabelle 1: Zentrale Annahmen der forstökonomischen Modelle von Dieter (2001), Knoke und Wurm (2006) und Loisel (2014) mit Einbeziehung natürlicher Risiken für Fagus sylvatica.

Table 2: Main strengths, limitations and suitability of the models by Dieter (2001), Knoke and Wurm (2006) and Loisel (2014).

Tabelle 2: Wichtigste Stärken, Schwächen und Eignung der Modelle von Dieter (2001), Knoke und Wurm (2006) und Loisel (2014).

As outlined in Tables 1 and 2, compared with Dieter’s and Knoke and Wurm’s empirically based survival curves and storm impact, Loisel’s formal stochastic treatment of storm probability and its link to tree height provides the more accurate tool when it comes to quantifying the impact of risk on land expectation value in pure Fagus sylvatica stands. This however leaves the question of how to address this risk in mixed stands, which seems to be the current trend of forest policy in Europe. For problems involving the introduction of Fagus sylvatica into conifer forests and the choice of the optimal Picea abies-Fagus sylvatica mix for the purposes of risk management, Knoke and Wurm’s portfolio framework provides the only avenue between the three models. This might be reflected in the current FWCI (Field-Weighted Citation Impact, i.e. citations relative to the world average for similar publications) values (Purkayastha et al., 2019) of these models (Dieter < 1, Loisel modestly > 1, Knoke and Wurm clearly > 2), which indicates that Loisel’s mathematically more complex model has so far achieved only moderate uptake compared with the simpler portfolio approach of Knoke and Wurm. This could be due to its narrower hazard focus (only storm risk and even-aged stands) and the higher technical threshold for implementation due to its complexity and mathematical formalism. With modern statistical software, simulation tools and AI-based modelling support, these barriers are increasingly surmountable.

Taken together, Tables 1 and 2 underline that Loisel’s (2014) model currently offers the most accurate framework for storm-exposed pure Fagus sylvatica stands, but Knoke and Wurm’s (2006) portfolio approach remains the only option among the three for modeling species-mixture and forest owner risk-preference. Dieter’s (2001) formulation lacks broad applicability but has the advantage of being mathematically straightforward and so it can be useful for simple, regional applications.

4.5 Next steps and future research

Limitations, such as higher technical complexity and demanding data requirements, that may have so far limited the uptake of mathematically more formal Faustmann-type models, are becoming less constraining as modern statistical software, simulation tools and even AI-based modelling are integrated at an ever-increasing rate into the economic and sylvicultural practices of modern forestry. In this context, future research could focus on testing models that are more complex and demanding in terms of calculation power, such as Loisel (2014) to examine their efficacy against the multitude of risks brought on by climate change, across different European regions and alternative climate and disturbance scenarios.

Future research should also explore adapting Loisel’s (2014) storm-risk framework, or a similar generalized Faustmann-type model for storm and timber price risk, to uneven-aged Fagus sylvatica stands. Further, a combination of approaches could achieve an even more complete and accurate framework for the economic valuation of Fagus sylvatica stands in mixed forests under climate change. Due to the generalized formulation of Loisel’s (2014) model, it could be possible to incorporate its method of addressing risk with Knoke and Wurm’s (2006) portfolio approach, in order to more accurately inform predictions on optimal Fagus sylvatica-Picea abies mixture. Such an integrated modelling framework lies beyond the scope of the present paper but might constitute a promising avenue for future research.

5 Conclusions

In conclusion, because of its particular vulnerability to storms and other natural hazards, Fagus sylvatica requires forest economic models that take into account its biological specificities and the increased uncertainty caused by climate change. The three approaches presented offer alternative paths for incorporating risk. with Loisel’s (2014) model emerging as the most suitable solution for Fagus sylvatica, both in terms of ecological realism and mathematical validity. The explicit incorporation of risk into the management of Fagus sylvatica in Europe is necessary in view of climate change and the increasing incidence of windthrow, fires and storms, but presupposes institutional provision in forestry law. The use of forest economic models in forest management — in particular models within the Faustmann tradition that incorporate climatic risks — would provide a well-documented framework for planning harvests and thinnings so as to protect the forest and valuable timber species such as Fagus sylvatica. Such a shift serves not only the optimisation of economic returns but also the protection of forest ecosystems, which are critical for mitigating the impacts of climate change.

At the same time, the comparison undertaken here does not support a single universally applicable model, because Loisel (2014) is intended for pure stands, while Knoke and Wurm (2006) address mixed forests. In theory, a judicious combination of Loisel’s risk formulation with Knoke and Wurm’s portfolio approach could yield a more complete framework that aligns with the increasingly adopted policy of mixing Fagus sylvatica into Picea abies stands across Europe and addresses risk both from the perspective of forest land valuation and risk aversion from forest owners.

References

Antonucci, S., Santopuoli, G., Marchetti, M., Tognetti, R., Chiavetta, U., & Garfì, V. (2021). What Is Known About the Management of European Beech Forests Facing Climate Change? A Review. Current Forestry Reports, 7(4), 321–333. https://doi.org/10.1007/s40725-021-00149-4

Binkley, C. S. (1993). Long-run Timber Supply: Price Elasticity, Inventory Elasticity, and the Use of Capital in Timber Production. Natural Resource Modeling, 7(2), 163–181. https://doi.org/10.1111/j.1939-7445.1993.tb00145.x

Bolte, A., Czajkowski, T., & Kompa, T. (2007). The north-eastern distribution range of European beech a review. Forestry, 80(4), 413–429. https://doi.org/10.1093/forestry/cpm028

Brazee, R. J., & Newman, D. H. (1999). Observations on recent forest economic research on risk and uncertainty. Journal of Forest Economics, 5, 193–200.

Bulte, E. H., & Van Kooten, G. C. (1999). Metapopulation dynamics and stochastic bioeconomic modeling. Ecological Economics, 30(2), 293–299. https://doi.org/10.1016/S0921-8009(98)00137-2

Dieter, M. (2001). Land expectation values for spruce and beech calculated with Monte Carlo modelling techniques. Forest Policy and Economics, 2(2), 157–166. https://doi.org/10.1016/S1389-9341(01)00045-4

Dittmar, C., Zech, W., & Elling, W. (2003). Growth variations of Common beech (Fagus sylvatica L.) under different climatic and environmental conditions in Europe—A dendroecological study. Forest Ecology and Management, 173(1–3), 63–78. https://doi.org/10.1016/S0378-1127(01)00816-7

Ellenberg, H. (1996). Vegetation Mitteleuropas mit den Alpen in ökologischer, dynamischer und historischer Sicht. Ulmer.

Elton, E. J., & Gruber, M. J. (1995). Modern portfolio theory and investment analysis (5th ed.). Wiley.

Faustmann, M. (1849). Calculation of the value which forest land and immature stands possess for forestry. Allgemeine Forst- und Jagdzeitung, 15, 441–455.

Fuchs, Z., Vacek, Z., Vacek, S., Černý, J., Cukor, J., Šimůnek, V., Gallo, J., & Hájek, V. (2025). Growth Responses of European Beech (Fagus sylvatica L.) and Oriental Beech (Fagus orientalis Lipsky) Along an Elevation Gradient Under Global Climate Change. Forests, 16(4), 655. https://doi.org/10.3390/f16040655

Geßler, A., Keitel, C., Kreuzwieser, J., Matyssek, R., Seiler, W., & Rennenberg, H. (2006). Potential risks for European beech (Fagus sylvatica L.) in a changing climate. Trees, 21(1), 1–11. https://doi.org/10.1007/s00468-006-0107-x

Girona-García, A., Badía-Villas, D., Jiménez-Morillo, N. T., De La Rosa, J. M., & González-Pérez, J. A. (2018). Soil C and N isotope composition after a centennial Scots pine afforestation in podzols of native European beech forests in NE-Spain. CATENA, 165, 434–441. https://doi.org/10.1016/j.catena.2018.02.023

Griess, V. C., & Knoke, T. (2013). Bioeconomic modeling of mixed Norway spruce—European beech stands: Economic consequences of considering ecological effects. European Journal of Forest Research, 132(3), 511–522. https://doi.org/10.1007/s10342-013-0692-3

Hanewinkel, M., Cullmann, D. A., Schelhaas, M.-J., Nabuurs, G.-J., & Zimmermann, N. E. (2013). Climate change may cause severe loss in the economic value of European forest land. Nature Climate Change, 3(3), 203–207. https://doi.org/10.1038/nclimate1687

Hanewinkel, M., Hummel, S., & Cullmann, D. A. (2010). Modelling and economic evaluation of forest biome shifts under climate change in Southwest Germany. Forest Ecology and Management, 259(4), 710–719. https://doi.org/10.1016/j.foreco.2009.08.021

Hanewinkel, M., Peltola, H., Soares, P., & González-Olabarria, J. R. (2010). Recent approaches to model the risk of storm and fire. Forest Systems, 19, 30–47. https://doi.org/10.5424/fs/201019S-9286

Holuša, J., Henzlová, I., Dvořáková, B., Resnerová, K., Šipoš, J., Holuša, O., Bláha, J., Berčák, R., Procházka, J., Trombik, J., & Fiala, T. (2025). Abundance of Taphrorychus bicolor in beech forests: Influence of forest size and optimal conditions. Forest Ecology and Management, 575, 122362. https://doi.org/10.1016/j.foreco.2024.122362

Houston Durrant, T., de Rigo, D., & Caudullo, G. (2016). Fagus sylvatica and other beeches in Europe: Distribution, habitat, usage and threats. In J. San-Miguel-Ayanz, D. de Rigo, G. Caudullo, T. Houston Durrant, & A. Mauri (Eds.), European Atlas of Forest Tree Species (p. e012b90+). Publications Office of the European Union.

Jump, A. S., Hunt, J. M., & Peñuelas, J. (2006). Rapid climate change‐related growth decline at the southern range edge of Fagus sylvatica. Global Change Biology, 12(11), 2163–2174. https://doi.org/10.1111/j.1365-2486.2006.01250.x

Kermavnar, J., Kutnar, L., & Marinšek, A. (2023). More losses than gains? Distribution models predict species-specific shifts in climatic suitability for European beech forest herbs under climate change. Frontiers in Forests and Global Change, 6, 1236842. https://doi.org/10.3389/ffgc.2023.1236842

Klemperer, W. D. (1996). Forest Resource Economics and Finance. McGraw-Hill.

Knoke, T., & Seifert, T. (2008). Integrating selected ecological effects of mixed European beech–Norway spruce stands in bioeconomic modelling. Ecological Modelling, 210(4), 487–498. https://doi.org/10.1016/j.ecolmodel.2007.08.011

Knoke, T., & Wurm, J. (2006). Mixed forests and a flexible harvest policy: A problem for conventional risk analysis? European Journal of Forest Research, 125(3), 303–315. https://doi.org/10.1007/s10342-006-0119-5

Kurz, W. A., Dymond, C. C., Stinson, G., Rampley, G. J., Neilson, E. T., Carroll, A. L., Ebata, T., & Safranyik, L. (2008). Mountain pine beetle and forest carbon feedback to climate change. Nature, 452(7190), 987–990. https://doi.org/10.1038/nature06777

Leuschner, C. (2020). Drought response of European beech (Fagus sylvatica L.)—A review. Perspectives in Plant Ecology, Evolution and Systematics, 47, 125576. https://doi.org/10.1016/j.ppees.2020.125576

Leuschner, C., Meier, I. C., & Hertel, D. (2006). On the niche breadth of Fagus sylvatica : Soil nutrient status in 50 Central European beech stands on a broad range of bedrock types. Annals of Forest Science, 63(4), 355–368. https://doi.org/10.1051/forest:2006016

Liepiņš, K., & Bleive, A. (2025). The Potential of European Beech (Fagus sylvatica L.) in the Hemiboreal Baltic Region: A Review. Forests, 16(1), 109. https://doi.org/10.3390/f16010109

Lindner, M., Maroschek, M., Netherer, S., Kremer, A., Barbati, A., Garcia-Gonzalo, J., Seidl, R., Delzon, S., Corona, P., Kolström, M., Lexer, M. J., & Marchetti, M. (2010). Climate change impacts, adaptive capacity, and vulnerability of European forest ecosystems. Forest Ecology and Management, 259(4), 698–709. https://doi.org/10.1016/j.foreco.2009.09.023

Loisel, P. (2014). Impact of storm risk on Faustmann rotation. Forest Policy and Economics, 38, 191–198. https://doi.org/10.1016/j.forpol.2013.08.002

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77–91.

Markuljaková, K., Mikoláš, M., Svitok, M., Meigs, G., Keeton, W., Kozák, D., Pavlin, J., Gloor, R., Kalaš, M., Ferenčík, M., Ralhan, D., Frankovič, M., Hofmeister, J., Dúhová, D., Mejstrík, M., Dušátko, M., Veber, A., Knír, T., & Svoboda, M. (2025). Rewilding beech-dominated temperate forest ecosystems: Effects on carbon stocks and biodiversity indicators. iForest – Biogeosciences and Forestry, 18(1), 1–9. https://doi.org/10.3832/ifor4600-017

Martinez Del Castillo, E., Zang, C. S., Buras, A., Hacket-Pain, A., Esper, J., Serrano-Notivoli, R., Hartl, C., Weigel, R., Klesse, S., Resco De Dios, V., Scharnweber, T., Dorado-Liñán, I., Van Der Maaten-Theunissen, M., Van Der Maaten, E., Jump, A., Mikac, S., Banzragch, B.-E., Beck, W., Cavin, L., … De Luis, M. (2022). Climate-change-driven growth decline of European beech forests. Communications Biology, 5(1), 163. https://doi.org/10.1038/s42003-022-03107-3

Moosmayer, H.-U. (2002). Langfristige regionale Waldbauplanung in Baden-Württemberg – Grundlagen und Ergebnisse. Landesforstverwaltung Baden-Württemberg.

Mpekiri, S., & Papaspyropoulos, K. G. (2026). Citation dynamics, thematic structure and temporal evolution of research on the Faustmann Forest Economics model (1962–2025). Forest Policy and Economics, 182, 103685. https://doi.org/10.1016/j.forpol.2025.103685.

Nocentini, S. (2009). Structure and management of beech (Fagus sylvatica L.) forests in Italy. iForest – Biogeosciences and Forestry, 2(3), 105–113. https://doi.org/10.3832/ifor0499-002

Övergaard, R., & Stener, L.-G. (2010). Current state of European beech (Fagus sylvatica L.) in Sweden. Communicationes Instituti Forestalis Bohemicae, 25, 242–247.

Papaspyropoulos, K. G., & Karamanolis, D. (2018). [New trends in Forest Economics: The case of Material Flow Cost Accounting]. Geotechnika Epistimonika Themata, 27(1), 47–56.

Peñuelas, J., & Boada, M. (2003). A global change‐induced biome shift in the Montseny mountains (NE Spain). Global Change Biology, 9(2), 131–140. https://doi.org/10.1046/j.1365-2486.2003.00566.x

Pflaumer, P. (1992). Investitionsrechnung. Oldenburg Verlag.

Rakotoarison, H., & Loisel, P. (2017). The Faustmann model under storm risk and price uncertainty: A case study of European beech in Northwestern France. Forest Policy and Economics, 81, 30–37. https://doi.org/10.1016/j.forpol.2017.04.012

Roibu, C.-C., Palaghianu, C., Nagavciuc, V., Ionita, M., Sfecla, V., Mursa, A., Crivellaro, A., Stirbu, M.-I., Cotos, M.-G., Popa, A., Sfecla, I., & Popa, I. (2022). The Response of Beech (Fagus sylvatica L.) Populations to Climate in the Easternmost Sites of Its European Distribution. Plants, 11(23), 3310. https://doi.org/10.3390/plants11233310

Schmidt, M., Hanewinkel, M., Kändler, G., Kublin, E., & Kohnle, U. (2010). An inventory-based approach for modeling single-tree storm damage—Experiences with the winter storm of 1999 in southwestern Germany. Canadian Journal of Forest Research, 40(8), 1636–1652. https://doi.org/10.1139/X10-099

Schwarzbauer, P., Braun, M., & Sekot, W. (2025). The Impact of Salvage Logging on the Supply of Roundwood Assortments from Austrian Forests – a Statistical Analysis. Austrian Journal of Forest Science / Centralblatt Für Das Gesamte Forstwesen, 142(4), 337–364.

Spanos, K. A., Skouteri, A., Gaitanis, D., Petrakis, P. V., Meliadis, I., Michopoulos, P., Solomou, A., Koulelis, P., & Avramidou, E. V. (2021). Forests of Greece, Their Multiple Functions and Uses, Sustainable Management and Biodiversity Conservation in the Face of Climate Change. Open Journal of Ecology, 11(04), 374–406. https://doi.org/10.4236/oje.2021.114026

Sperlich, D., Hanewinkel, M., & Yousefpour, R. (2024). Aiming at a moving target: Economic evaluation of adaptation strategies under the uncertainty of climate change and CO2 fertilization of European beech (Fagus sylvatica L.) and Silver fir (Abies alba Mill.). Annals of Forest Science, 81(1), 4. https://doi.org/10.1186/s13595-023-01215-6

Spiecker, H., Hansen, J., Klimo, E., Skovsgaard, J. P., Sterba, H., & von Teuffel, K. (2004). Norway Spruce Conversion: Options and Consequences (1st ed). BRILL.

Špoula, J., Véle, A., & Neudertová Hellebrandová, K. (2024). Influence of Elevation and Stand Age on the Abundance of the Beech Bark Beetle (Taphrorychus bicolor Her.) and Its Potential Threat to Beech Stands. Forests, 15(9), 1595. https://doi.org/10.3390/f15091595

Tahvonen, O., & Viitala, E.-J. (2006). Does Faustmann Rotation Apply to Fully Regulated Forests? Forest Science, 52(1), 23–30. https://doi.org/10.1093/forestscience/52.1.23

Tarp, P., Helles, F., Holten-Andersen, P., Bo Larsen, J., & Strange, N. (2000). Modelling near-natural silvicultural regimes for beech – an economic sensitivity analysis. Forest Ecology and Management, 130(1–3), 187–198. https://doi.org/10.1016/S0378-1127(99)00190-5

Uhl, B., Schall, P., & Bässler, C. (2025). Achieving structural heterogeneity and high multi-taxon biodiversity in managed forest ecosystems: A European review. Biodiversity and Conservation, 34(9), 3327–3358. https://doi.org/10.1007/s10531-024-02878-x

Vujanovic, V., Kim, S. H., Latinovic, J., & Latinovic, N. (2020). Natural Fungicolous Regulators of Biscogniauxia destructiva sp. Nov. That Causes Beech Bark Tarcrust in Southern European (Fagus sylvatica) Forests. Microorganisms, 8(12), 1999. https://doi.org/10.3390/microorganisms8121999

Zeng, H., Peltola, H., Väisänen, H., & Kellomäki, S. (2009). The effects of fragmentation on the susceptibility of a boreal forest ecosystem to wind damage. Forest Ecology and Management, 257(3), 1165–1173. https://doi.org/10.1016/j.foreco.2008.12.003